The IRS accepted just 31% of Offers in Compromise in fiscal year 2023. That’s roughly 17,000 approved out of 54,000 filed. The rejected 69% share a pattern we see constantly at Austin & Larson Tax Resolution. Incomplete documentation, math errors on the 433-A (OIC), and bad RCP calculations kill most Offers. These problems end cases before they get a fair review.

Every tip below targets a specific reason the IRS returns or rejects Offers. They’re ordered by impact, not alphabetically. The first three account for the majority of preventable rejections.

1. Calculate your Reasonable Collection Potential before you file

Most OIC rejections aren’t judgment calls. They’re math.

The IRS uses a formula called Reasonable Collection Potential (RCP). RCP equals your asset equity plus future income over the collection period. For a lump sum offer, that period covers 12 months. For periodic payment offers, it covers 24 months.

Submit an Offer amount below your RCP and the IRS rejects it automatically. Run the calculation yourself using the IRS OIC Pre-Qualifier Tool first. Do this before spending the $205 application fee.

Compare your numbers against IRS Collection Financial Standards for allowable living expenses. These are published tables, not negotiable figures. Your mortgage, food, and transportation allowances all have caps. Exceed those caps without justification and the IRS recalculates your RCP higher.

This step separates approved Offers from wasted filing fees.

2. Organize every document around the 433-A (OIC) line items

The Offer Specialist assigned to your case manages dozens of files. They won’t spend extra time matching random bank statements to expense categories. Your job is to eliminate that friction completely.

Label every supporting document with the exact line number from Form 433-A (OIC). If line 36 claims $1,400 in monthly housing costs, paper clip your mortgage statement to a note. Write “Line 36, Housing: $1,400/month” on that note. Highlight the relevant figure on the statement itself.

This sounds tedious. It’s the single easiest way to get the Specialist working with you. Agents who verify your numbers quickly allow borderline expenses more often. Agents digging through a messy stack do not.

3. Attach complete supporting documentation with your initial submission

An incomplete package triggers an information request from the IRS. That burns 30 to 45 days of your processing window. It also tells the Specialist your file will require extra work.

At minimum, include three months of all bank statements from every account. Add utility bills, mortgage or rent verification, and vehicle loan statements with titles. Include proof of health and life insurance premiums. Attach recent pay stubs or profit and loss statements if you’re self-employed.

If you have retirement accounts, include the most recent statements. The IRS will find them regardless of whether you disclose them. Including them upfront shows transparency and protects your credibility.

Your goal is zero follow up requests on the initial submission.

4. Be accurate because the IRS will cross reference everything

The IRS accesses your wage transcripts, 1099 filings, and bank deposit records first. They run your Social Security number through the Automated Underreporter system. Every third party report gets compared against your 433-A (OIC).

A $3,000 monthly deposit that doesn’t appear as income creates a credibility problem. Even if it’s a transfer between your own accounts, you carry the burden. That unexplained deposit can taint every other number on your application.

When in doubt, include it and explain it. An Offer with a detailed explanation note raises zero flags. An Offer that omits known income can trigger a fraud referral under 26 U.S.C. § 7206. The consequences of unresolved tax issues multiply fast once credibility breaks down.

5. Sign every form and submit your payment correctly

This is the most preventable rejection reason in the entire OIC process. Both Form 656 and Form 433-A (OIC) require signatures. Joint Offers require both spouses to sign every form.

You’ll also submit the $205 application fee with your initial payment. For a lump sum Offer, that initial payment equals 20% of the total Offer amount. Lump sum means paid in 5 or fewer installments. For a periodic payment Offer, submit your first proposed monthly payment.

Make sure the funds clear your bank account. A bounced check means your entire Offer gets returned. You’ll lose time and need to refile from scratch.

One exception exists: the low income certification on Form 656, Section 1. It waives both the fee and the initial payment. You qualify if household income falls at or below 250% of the federal poverty guidelines.

6. Respond to IRS contact within 14 days

Once your Offer reaches a Specialist, they’ll contact you by phone, mail, or both. Phone contact typically allows 14 days for your response. Mailed requests usually allow 30 days.

Miss the first contact window and the IRS can return your Offer without appeal rights. That happens regularly. It’s not a technicality.

Set up a dedicated system for tracking IRS mail. If you’ve moved or changed phone numbers since filing, update the IRS using Form 8822. A qualified Offer that goes to the wrong address produces the same result as no Offer.

7. Respond to additional information requests fast

When the Specialist requests additional documents, you’ll typically get 14 to 30 days. Don’t use all of it. Respond within a week if you can.

Speed matters for a reason most applicants don’t realize. OIC processing follows an internal timeline at the IRS. The IRS must decide within two years of the received date. Specialists manage their caseloads against that clock constantly. A responsive applicant moves through the pipeline faster at every stage.

Apply the same labeling system from Tip 2 when sending additional information. Reference the specific items the Specialist requested by name. Send everything in one package rather than piecemeal.

8. Always send copies, never originals

The IRS does not return original documents. Period.

Send clear, legible copies of everything you submit. This covers your initial Offer forms, every supporting document, and every follow up response. Keep your own complete copy of the entire Offer package.

When the Specialist calls to discuss your case, you need the same documents in front of you. If you end up in Appeals, you’ll need to reconstruct the full record. Having organized copies on hand makes that process straightforward. Losing originals to the IRS turns it into a nightmare.

9. Get everything in writing

Verbal agreements with IRS employees carry no weight. If a Specialist approves an expense by phone, that statement means nothing later. A different agent reviewing the file won’t know about it.

Request written confirmation of any verbal communication. If the Specialist asks for information by phone, ask for a written follow up. That request should list the specific items needed and the deadline.

Send your responses in writing and keep copies of each one. This builds a documented record that protects your Offer through every stage. Initial evaluation, potential rejection, and the Appeals process all benefit from a clear paper trail.

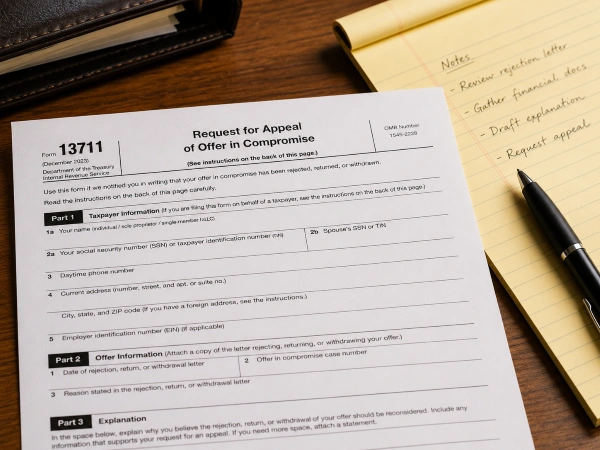

10. If your Offer gets rejected, appeal it

An OIC rejection isn’t the end. You have 30 days from the rejection letter date to file Form 13711. That’s the Request for Appeal of Offer in Compromise.

Appeals assigns your case to a completely new person. This reviewer wasn’t involved in the original decision. Appeals Officers carry broader authority than Offer Specialists. They can weigh factors the initial reviewer dismissed.

Some Offer Specialists reject more cases than others. That’s a reality of the system, not a reflection of your case’s merit. File the appeal. The worst outcome is the same answer you already have.

After acceptance: don’t default your Offer

Getting an Offer accepted is only half the battle. You’ll have 5 months (lump sum) or 24 months (periodic payment) to pay the remaining balance. Miss a payment and the IRS can default your Offer. That reinstates the full original debt plus accrued penalties and interest.

You must also file all tax returns on time for five years after acceptance. Every tax balance during that compliance period must stay paid in full. A single unfiled return or unpaid balance can void your Offer entirely.

If you can’t meet the Offer terms, contact the IRS or your representative immediately. An installment agreement on a current year balance beats defaulting your entire OIC. Understanding whether an OIC affects your credit helps you plan for the five year compliance window.

The real difference between acceptance and rejection

The gap between the 31% that get accepted and the 69% that don’t usually isn’t financial. It’s preparation quality. An Offer in Compromise is the most powerful debt resolution tool the IRS offers. It’s also the most procedurally unforgiving.

If you’re considering an OIC, contact Austin & Larson Tax Resolution for a consultation. Our team of IRS Enrolled Agents, CPAs, and Tax Attorneys handles OIC cases across Michigan. We’ll tell you whether you qualify and calculate your realistic Offer amount before you spend a dollar.

FAQs

What is an Offer in Compromise with the IRS?

An Offer in Compromise lets a taxpayer settle IRS tax debt for less than the full amount owed. The IRS evaluates your income, expenses, and assets to determine the minimum amount they’ll accept.

How long does the IRS take to process an Offer in Compromise?

Most Offers take 6 to 12 months for the IRS to review and decide. Processing time depends on the complexity of your financials and how quickly you respond to information requests.

What is the $205 OIC application fee?

The IRS charges a $205 nonrefundable fee when you submit your Offer in Compromise. This fee gets waived if your household income falls at or below 250% of the federal poverty guidelines.

What happens if the IRS rejects my Offer in Compromise?

You have 30 days from the rejection date to file Form 13711 and request an appeal. A new Appeals Officer reviews your case independently from the original Offer Specialist.

Can I still file an Offer in Compromise if I have unfiled tax returns?

You must file all required tax returns before the IRS will consider your Offer. Complete your delinquent returns first, then submit your OIC application with full documentation.

What is Reasonable Collection Potential?

Reasonable Collection Potential (RCP) is the IRS formula for calculating the minimum Offer amount they’ll accept. It equals the equity in your assets plus your expected future income over the collection period.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments