The IRS audits roughly 0.4% of individual returns each year, but taxpayers who handle their own audits lose an average of 30% more in denied deductions than those who hire professional representation. That gap isn’t about having better records. It’s about understanding what the auditor is actually looking for, what you’re legally required to hand over, and what conversations can hurt you without you realizing it.

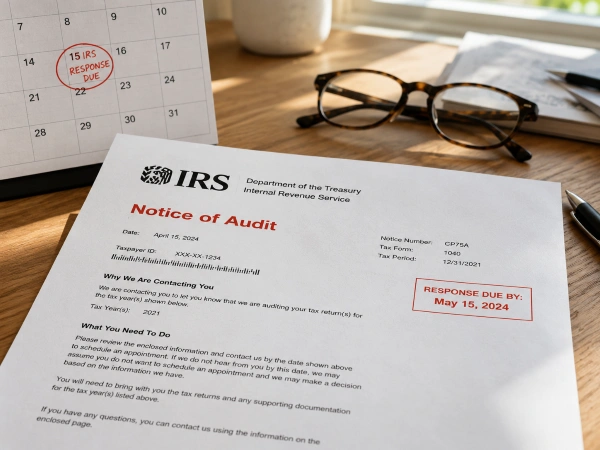

If you’ve received an IRS audit notice (typically Letter 2202 or Letter 3572), you have a narrow window to respond. Before you call the number on that letter or start gathering documents, get tax audit help from a qualified representative: an enrolled agent, CPA, or tax attorney. That single decision shapes everything that follows.

What triggers an IRS audit and how far back can they go?

The IRS selects returns for audit through its Discriminant Inventory Function (DIF) scoring system, which flags returns that deviate from statistical norms for your income bracket and filing type. Common triggers include unusually high deductions relative to income, unreported 1099 income, large charitable contributions, and home office claims.

Under IRC Section 6501, the IRS has three years from the filing date to audit most returns. That window extends to six years if the IRS suspects you’ve underreported gross income by more than 25%. And there’s no statute of limitations at all for fraud or unfiled returns.

Once selected, you’ll receive a mailed notice. The IRS does not initiate audits by phone or email. The audit will take one of two forms: a correspondence audit handled entirely by mail, or an in-person audit conducted at an IRS office, your home, or your place of business.

Why handling your own audit is a costly mistake

An IRS auditor is trained to do one thing: maximize the government’s tax assessment. The process is adversarial by design, even when the auditor seems friendly. This is where unrepresented taxpayers get burned.

Auditors conduct what’s called a “lifestyle interview” during in-person audits. They’ll ask about your daily routine, spending habits, vehicles, vacations, and children’s schools. These questions feel conversational. They’re not. The auditor is cross-referencing your answers against your reported income to identify discrepancies. A casual mention of a family vacation to Europe can trigger scrutiny of your entire reported income if it doesn’t align with what you claimed.

Many taxpayers walk into an audit confident their return is correct, find the auditor pleasant and helpful, and then receive an examination report (Form 4549) weeks later with most of their deductions denied and a balance of taxes, interest, and penalties they didn’t expect. By that point, the damage is done. Statements made during the interview are already in the case file.

A qualified tax representative eliminates this risk by handling all IRS contact on your behalf. Under IRS Circular 230, enrolled agents, CPAs, and tax attorneys have the legal right to represent you without you being present. The auditor talks to your representative, not to you.

What the auditor will request from you

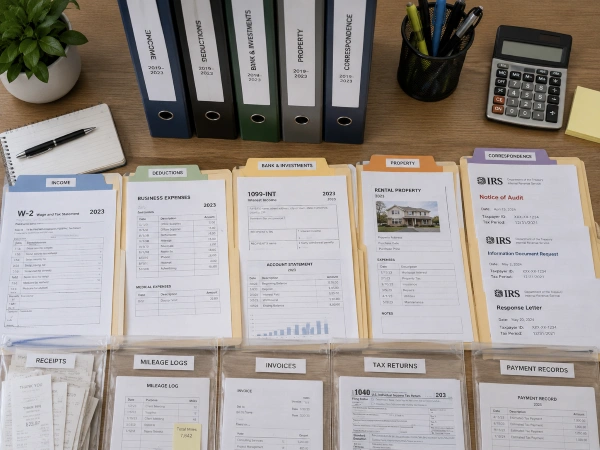

For each line item under review, the IRS will request substantiation, the documentation proving you earned what you reported and spent what you deducted. Expect requests for:

- Bank statements. The auditor can subpoena these directly from your financial institution if you don’t provide them, so withholding them isn’t a viable strategy.

- Receipts and canceled checks. For every deduction claimed, you’ll need proof of payment and business purpose.

- Contracts, invoices, and mileage logs. Particularly for self-employment income, home office deductions, and vehicle expense claims.

- Third-party records. Mortgage statements, medical bills, childcare provider statements, and charitable donation acknowledgment letters.

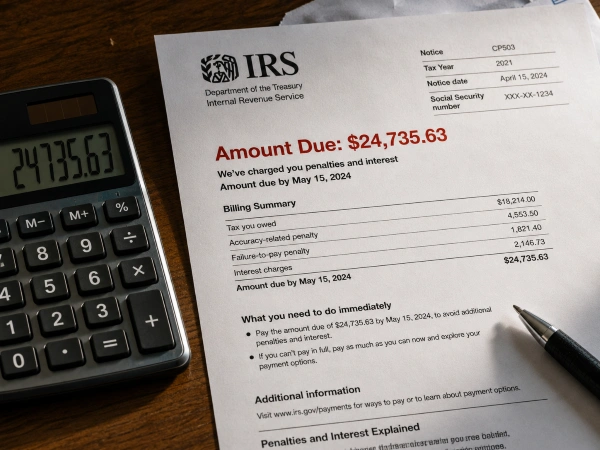

The auditor will set deadlines for producing these records. Those deadlines are legally enforceable. If you can’t produce documentation by the deadline and don’t request an extension in writing, the auditor will issue a report denying any unsupported deductions, regardless of whether those deductions were legitimate.

This is the second-most common way taxpayers lose audits. Not because their return was wrong, but because they couldn’t organize the volume of records required within the time allowed.

How to protect yourself during an IRS audit

- Hire representation before you respond to anything. Your representative can request additional time to respond to the initial notice, review your records for any issues before the auditor sees them, and develop a strategy for the audit. This isn’t about hiding anything. It’s about presenting your documentation in the strongest possible way. Austin & Larson Tax Resolution offers free initial consultations to review your audit notice and outline your options.

- Never send original documents to the IRS. This sounds obvious, but it happens constantly. Whether you’re mailing records or handing them over in person, provide copies only. The IRS will not return your originals. If they lose them (and they do), you’ll have no backup for your deductions.

- Organize your documentation by line item, not by date. Don’t show up with a box of receipts. Arrange your records to match the specific items the auditor requested, with a cover sheet summarizing totals for each category. An auditor who has to sort through a pile of unsorted documents is an auditor who’s more likely to miss deductions in your favor and less likely to give you the benefit of the doubt.

- Track every deadline on every notice. IRS audit notices carry deadlines for producing documents, filing appeals, and extending the assessment statute (the time the IRS has to finalize your audit). Missing a deadline to file Form 12203 (Request for Appeals Review), for example, can forfeit your right to dispute the auditor’s findings without going to Tax Court. Read every notice the day it arrives and calendar every date.

- Put everything in writing and send it certified. Phone conversations with the IRS are not reliably documented. Any request you make, whether deadline extensions, clarification of what’s being audited, or challenges to the auditor’s findings, should be submitted in writing via certified mail with return receipt. This creates a paper trail that protects you if the IRS claims they never received something. For a detailed walkthrough of what to do the moment you receive your notice, see our guide on the steps to take after receiving an IRS audit.

What to do if you disagree with the audit results

You’re not stuck with the auditor’s findings. After receiving the examination report, you have 30 days to file an appeal with the IRS Office of Appeals, an independent division separate from the examination group that conducted your audit. Appeals conferences resolve roughly 80 to 90 percent of cases without going to court, and the outcomes frequently favor the taxpayer when new documentation or legal arguments are presented.

If the appeals process doesn’t resolve the dispute, you can petition the U.S. Tax Court within 90 days of receiving a Statutory Notice of Deficiency (the “90-day letter”). Tax Court is the only venue where you can challenge the IRS’s assessment without paying the disputed amount first.

The worst thing you can do is ignore an unfavorable audit result and hope it goes away. Unpaid audit assessments accrue interest and penalties, and the IRS has 10 years to collect. That clock doesn’t start until the assessment is finalized.

The real cost of going unrepresented

Tax audit representation typically costs between $2,000 and $10,000 depending on the complexity of the audit. That’s a meaningful expense. But taxpayers who go unrepresented routinely see denied deductions, penalties, and interest charges that dwarf the cost of hiring someone. The math almost always favors getting help, especially when the IRS is questioning deductions worth tens of thousands of dollars.

An audit isn’t a conversation. It’s a legal proceeding with rules, deadlines, and consequences. Treat it like one.

FAQs

What triggers an IRS audit?

The IRS uses its Discriminant Inventory Function (DIF) scoring system to flag returns that deviate from statistical norms for your income level and filing type. Common triggers include unusually high deductions relative to income, unreported 1099 income, large charitable contributions, and home office claims.

How far back can the IRS audit my tax returns?

The IRS can audit returns filed within the last three years under IRC Section 6501. That window extends to six years if gross income is underreported by more than 25%, and there is no statute of limitations for fraud or unfiled returns.

Should I handle my own IRS audit without professional help?

Taxpayers who represent themselves consistently lose more in denied deductions than those with professional representation. An enrolled agent, CPA, or tax attorney can represent you under IRS Circular 230 and handle all communication with the auditor on your behalf.

What documents does the IRS request during an audit?

The IRS requests substantiation for every line item under review, including bank statements, receipts, canceled checks, contracts, invoices, and mileage logs. Auditors can subpoena bank records directly from your financial institution, so withholding them isn’t a viable strategy.

What happens if I can’t gather my documents by the IRS deadline?

You can request a deadline extension in writing before the deadline passes, and auditors will often grant reasonable extensions. If you miss a deadline without requesting one, the auditor can deny all unsupported deductions regardless of whether they were legitimate.

What can I do if I disagree with IRS audit results?

You have 30 days after receiving the examination report to file an appeal with the IRS Office of Appeals, and 90 days after receiving a Statutory Notice of Deficiency to petition U.S. Tax Court. Tax Court is the only venue where you can challenge the assessment without paying the disputed amount first.

How much does tax audit representation cost?

Tax audit representation typically costs between $2,000 and $10,000 depending on audit complexity. That expense is almost always less than the denied deductions, penalties, and interest charges that unrepresented taxpayers face.

Does being audited mean I did something wrong?

No. Returns are selected through statistical scoring, random selection, or because they’re linked to another taxpayer already under audit, and many audits result in no changes when proper documentation is provided.

Recent Comments