Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 29, 2026

The single biggest reason tax returns get delayed, filed wrong, or leave money on the table is missing paperwork. Not bad math. Not software glitches. Missing documents.

You need three categories of records to prepare your tax return: income documents (what you earned), deduction and credit documents (what reduces your tax), and personal identification. That’s the framework. Everything else is detail.

To prepare a federal tax return, you need W-2s from every employer, all 1099 forms reporting other income, records of deductible expenses, Social Security numbers for yourself and any dependents, and your prior-year return for reference. Gathering these before you sit down to file (or before you meet with a preparer) cuts the typical filing time in half and reduces errors that trigger IRS notices.

This article covers the full checklist for 2026 filing (2025 tax year), including new forms and deductions from the One Big Beautiful Bill Act signed in mid-2025. We won’t cover state-specific requirements. Those vary, and your state’s revenue department website is the better source for those details.

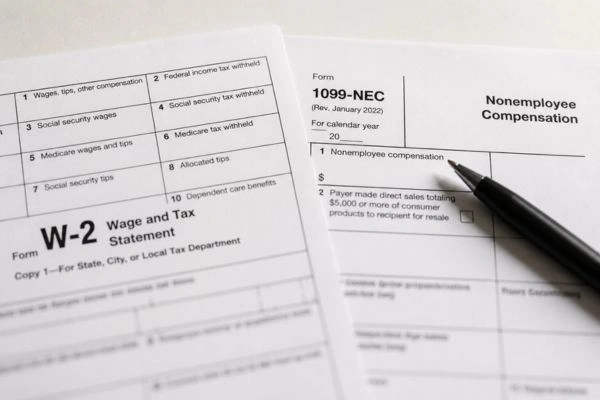

Income Documents Every Filer Needs

Every dollar of income needs a matching document. The IRS already has copies of most of these forms because employers and financial institutions send them directly. If your tax return doesn’t match what the IRS has on file, you’ll get a notice.

For W-2 employees, you need a W-2 from every employer you worked for during the year. If you worked two jobs, that’s two W-2s. Sounds obvious, but I’ve seen people forget about a job they left in February.

Beyond W-2s, here’s what to collect based on your situation:

- 1099-NEC for freelance or independent contractor income over $600

- 1099-K for payment app and marketplace income (the reporting threshold for 2025 returns is $2,500, down from $5,000 the prior year)

- 1099-INT and 1099-DIV for bank interest and stock dividends

- 1099-R for retirement account distributions (pensions, IRAs, 401(k) withdrawals)

- SSA-1099 for Social Security benefits received

- 1099-G for unemployment compensation or state tax refunds

- 1099-C for cancelled or forgiven debt (yes, the IRS counts this as income)

- 1099-DA for cryptocurrency and digital asset transactions (new reporting requirement for 2025 tax year)

- Schedule K-1 if you’re a partner in a business or received trust income

If you’re missing any of these by early February, contact the issuer directly. You can also pull your IRS wage and income transcript using the IRS online transcript tool to see what’s been reported under your Social Security number.

What Do Self-Employed and Gig Workers Need?

If you earn income outside of a traditional W-2 job, your document list is longer. And the stakes are higher, because the IRS doesn’t withhold taxes from this income. You’re responsible for tracking every dollar in and every deductible dollar out.

You’ll need all 1099-NEC and 1099-K forms, plus your own records for any income that falls below reporting thresholds. Just because a client didn’t send a 1099 doesn’t mean the income isn’t taxable.

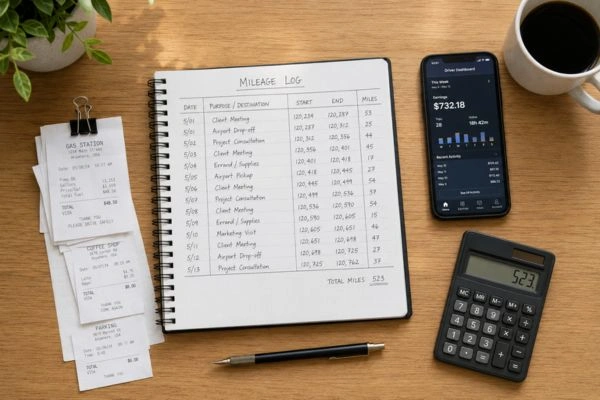

For deductions, keep records of business expenses: mileage logs, home office measurements and costs, equipment purchases, software subscriptions, supplies, and professional development. If you made quarterly estimated tax payments during the year, you’ll need your 1040-ES payment records or bank statements showing those payments.

I’ve worked with self-employed clients who lost thousands in deductions because they didn’t track mileage. The IRS standard mileage rate for 2025 is 70 cents per mile for business use. If you drove 15,000 miles for work, that’s $10,500 in deductions you’d miss without a log. A simple spreadsheet or mileage app is worth more than most people realize.

Deduction and Credit Documents That Save You Money

Deductions reduce your taxable income. Credits reduce your actual tax bill dollar for dollar. Both require documentation.

For homeowners: Form 1098 showing mortgage interest paid, property tax bills, and receipts for energy-efficient home improvements (solar panels, heat pumps, and similar upgrades may qualify for credits under the Inflation Reduction Act provisions still in effect).

For parents: Social Security numbers and birth dates for every dependent, childcare provider name and tax ID number with total paid, and Form 1098-T from colleges or universities if you’re claiming education credits. The Child Tax Credit also increased under the One Big Beautiful Bill Act. Verify current amounts with your preparer.

For healthcare: Form 1095-A if you bought insurance through the Marketplace, plus records of out-of-pocket medical expenses. Medical expenses are only deductible if they exceed 7.5% of your adjusted gross income, so most filers won’t benefit here unless they had a major medical event.

For charitable giving: receipts for cash donations, written acknowledgment from the organization for gifts of $250 or more, and records of donated goods with estimated fair market values.

Does Itemizing Still Make Sense in 2026?

This is the question the original version of this article never asked. And it matters more than any single document on the list.

The standard deduction for the 2025 tax year (filed in 2026) is $15,000 for single filers and $30,000 for married couples filing jointly. Those numbers increased under the One Big Beautiful Bill Act, which made the 2017 Tax Cuts and Jobs Act provisions permanent and added inflation adjustments.

If your total itemized deductions (mortgage interest, state and local taxes up to the SALT cap, charitable gifts, medical expenses) don’t exceed those thresholds, itemizing doesn’t help you. Roughly 87% of filers take the standard deduction, according to IRS filing data. For those people, half the documents on a typical “tax checklist” article are irrelevant.

My recommendation: add up your mortgage interest (from Form 1098), property taxes, state income taxes, and charitable donations. If the total is under $15,000 (single) or $30,000 (joint), take the standard deduction and don’t waste time gathering receipts for items that won’t affect your tax return.

The One Big Beautiful Bill Act also introduced new above-the-line deductions that apply regardless of whether you itemize: up to $25,000 in tip income, certain overtime pay, an extra $4,000 for seniors, and car loan interest on domestically assembled vehicles. These are new for 2025 tax returns, and they reduce your adjusted gross income directly.

What If You’re Missing Tax Documents?

Don’t wait forever. Most W-2s and 1099s are due to you by January 31. If it’s mid-February and you’re still missing one, contact the employer or institution first. If that doesn’t work, call the IRS at 800-829-1040 and they can send you a substitute.

You can also request your IRS transcript (Form 4506-T) to see exactly what income has been reported. I recommend this for anyone who had unfiled returns from prior years and needs to reconstruct records. Transcripts won’t show deductions, but they’ll confirm every income form on file.

If you lost receipts for deductions, bank and credit card statements can serve as backup documentation. The IRS accepts these as supporting records as long as the expense, date, and amount are clear.

Documents Most Filers Forget

After seeing hundreds of returns, these are the items that get missed most often:

- 1099-INT from savings accounts earning even small amounts of interest. Banks report anything over $10.

- Gambling winnings reported on W-2G (or unreported winnings you’re supposed to self-report).

- HSA contribution records (Form 5498-SA) and distribution records (Form 1099-SA).

- Student loan interest (Form 1098-E), which is deductible up to $2,500 even if you don’t itemize.

- Prior-year state tax refunds (1099-G), which may be taxable if you itemized the prior year.

- Cancelled debt (1099-C), which people assume isn’t taxable. It usually is.

One more that catches people off guard: if you sold a home, stocks, or crypto during the year, you need your original purchase price (cost basis) to calculate gains. Without it, the IRS assumes your basis is zero, and your tax bill jumps.

Keeping Records After You File

Filing your return doesn’t mean you can shred everything. The IRS can audit returns going back three years from the filing date. If they suspect you underreported income by more than 25%, that window extends to six years.

Keep all supporting documents (W-2s, 1099s, receipts, bank statements) for at least three years. Keep records related to property purchases, home improvements, and retirement contributions longer, because you’ll need them when you eventually sell or withdraw.

Store digital copies alongside paper. A photo of a receipt saved to a cloud folder takes 10 seconds and has saved more than a few of our clients from headaches during an IRS audit.

If your tax situation is complicated, or if you have unresolved IRS issues from prior years, getting organized now makes everything easier for the team handling your case.

Frequently Asked Questions

What are the most important documents needed to prepare a tax return?

At minimum, you need W-2s from all employers, any 1099 forms (for freelance income, interest, dividends, retirement distributions, and gig work), Social Security numbers for yourself and dependents, and your prior-year tax return. If you own a home, you’ll also need Form 1098 for mortgage interest and your property tax bills.

When should I receive my W-2 and 1099 forms?

Employers and financial institutions must send W-2s and most 1099s by January 31. If you haven’t received yours by mid-February, contact the issuer directly. You can also request an IRS wage and income transcript to see what’s been reported under your Social Security number.

Do I need receipts if I take the standard deduction?

For most deductions, no. The 2025 standard deduction is $15,000 for single filers and $30,000 for married couples filing jointly. About 87% of filers take the standard deduction. If your itemizable expenses fall below these thresholds, receipt gathering for those items won’t affect your return. Keep records for above-the-line deductions like student loan interest and self-employment expenses, which apply regardless.

What documents do self-employed workers need for taxes?

All 1099-NEC and 1099-K forms, records of business expenses (mileage logs, receipts, bank statements), home office measurements and costs if applicable, and records of quarterly estimated tax payments (1040-ES). The IRS standard mileage rate for 2025 is 70 cents per mile, so a mileage log alone can be worth thousands in deductions.

What new tax documents are required for 2026 filing?

The 2025 tax year introduced Form 1099-DA for cryptocurrency and digital asset transactions. The One Big Beautiful Bill Act also created new above-the-line deductions for tip income (up to $25,000), certain overtime pay, an additional $4,000 for seniors, and car loan interest on domestically assembled vehicles. You’ll need pay stubs or employer records to support these claims.

How long should I keep tax documents after filing?

The IRS can audit returns up to three years from the filing date. If they suspect underreporting of more than 25%, the window extends to six years. Keep all W-2s, 1099s, receipts, and bank statements for at least three years. Property and investment records should be kept longer, since you’ll need original purchase prices when you sell.

What if I lost tax documents I need to file?

Request an IRS transcript (Form 4506-T) to see all income reported under your Social Security number. For deductions, bank and credit card statements can serve as backup documentation. If you’re reconstructing records for multiple years of unfiled returns, working with a tax resolution professional is the fastest path.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments