Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: June 21, 2026

Most people who owe back taxes qualify for an IRS installment agreement, even if they can’t pay it at once. If you owe $50,000 or less and have filed every required return, the IRS reports that more than 90% of individual taxpayers can set up its Simple Payment Plan. It comes down to three things. Filing is current, your balance fits the limit, and you pick a payment you can sustain.

An IRS installment agreement is a written deal that lets you pay a tax balance in fixed monthly amounts instead of all at once. Federal law lets the IRS accept payments over time. While the plan is active and you stay current, the IRS holds off on levies and other collection.

How Do You Qualify for an IRS Installment Agreement?

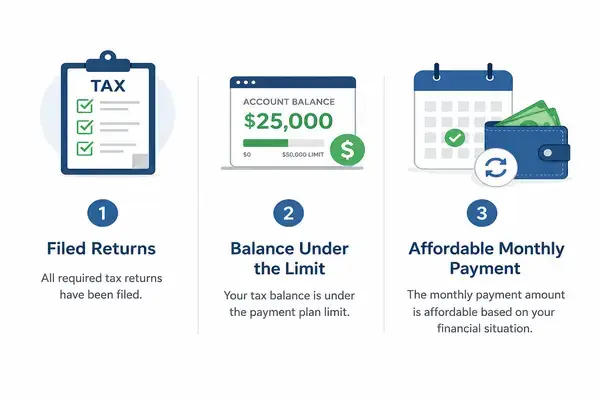

You qualify when three boxes are checked. Every required return is filed, your total balance fits the IRS limits, and your payment matches what you can afford.

File Every Required Return First

This is the one that trips people up. The IRS won’t approve a plan while you have unfiled returns out there. If you’re behind, getting your past-due returns filed is step one, since one missing year can hold up the request.

How Much Can You Owe and Still Qualify?

Your total balance (tax, penalties, and interest) decides which plan you can request. A short-term plan gives you up to 180 days to pay in full with no setup fee if you owe under $100,000. The long-term Simple Payment Plan spreads payments over years for balances of $50,000 or less. The IRS publishes the balance limits for online approval.

| Plan type | You can owe | Time to pay | Setup fee | Financial review? |

| Short-term plan | Under $100,000 | Up to 180 days | $0 | Usually none |

| Simple Payment Plan | $50,000 or less | Up to 72 months | $22 online with direct debit | Usually none |

| Standard installment agreement | Above the simple limits | Up to the collection deadline | Up to $178 | Yes, Form 433 |

Source: IRS payment plan rules, 2026.

Setup fees depend on how you apply. The cheapest route is online with direct debit, around $22. Apply by phone or mail and it climbs toward $178. If your income is under 250% of the federal poverty guidelines, those fees can be cut or waived, which for one person in 2026 means income near $39,900. The right installment agreement option depends on your balance.

Stay Current While the Plan Runs

Approval isn’t the finish line. You still have to file and pay everything new on time while the agreement runs. Let a fresh balance pile up and they can cancel it. A surprise bill next April can undo months of on-time payments, so keep your withholding accurate.

Pick a Monthly Payment You Can Actually Afford

Here’s where I push back on the usual advice. Everyone says “just set up the plan,” but the number you choose matters more than approval. For simple online plans the IRS won’t dig into your finances, but owe more than the limits or ask for a very low payment and they’ll want Form 433 details.

The costliest mistake isn’t a denial. It’s people who panic and promise a higher monthly payment than they can actually manage. They default, collection restarts, and reinstatement fees pile on. If a real payment would leave you short on rent, a temporary hardship status can beat a plan you’re set up to fail.

One upside almost nobody mentions: the day your plan goes active, the failure-to-pay penalty drops from 0.5% a month to 0.25%. Interest still runs (federal short-term rate plus 3%, compounded daily), so paying faster costs less.

A Few Things That Stall Approval

Two things put approval on hold, an open bankruptcy and a history of defaulting on a past plan. While a bankruptcy case is active, the IRS handles collection differently, and a new installment agreement usually waits until it wraps up. Defaulted before? Expect a closer review first.

Why Checking Early Saves You Money

Checking early protects you from two costly errors. Wait too long and the IRS restarts collection; apply wrong and you overpay in fees. Acting now, and leaning on experienced guidance when a case gets complicated, keeps a fixable problem from turning into a levy.

Your IRS Installment Agreement Eligibility Checklist

You’re likely eligible for an IRS installment agreement if you can check these three boxes:

1. Every required tax return is filed and up to date.

2. Your total balance is under $100,000 for a short-term plan, or $50,000 or less for the long-term Simple Payment Plan.

3. You can make a realistic monthly payment and stay current on future taxes.

Check all three and the IRS online system usually approves you in minutes. Miss one and you still have options. If your balance is large, your income swings, or you’ve defaulted before, bring in Austin & Larson, a Michigan tax resolution team that handles these daily. The worst move with an IRS installment agreement is waiting until a levy makes the decision for you.

FAQs

Can you set up an IRS installment agreement if you haven’t filed your latest return?

No. The IRS requires you to be current on all required returns before it approves an installment agreement. One unfiled year can hold up the entire request, so file any missing returns first, then apply for a plan.

Does an IRS installment agreement stop collection right away?

Generally yes. While your request is pending and after the plan is approved, the IRS pauses new levies as long as you keep the terms. A federal tax lien that was already filed can stay in place, and interest and penalties keep running until the balance is paid in full.

What happens if you default on an IRS installment agreement?

The IRS sends Notice CP523 and can terminate the plan, restart collection such as levies and liens, and apply future refunds to your balance. Penalties and interest keep adding up. You generally have 30 days to fix the missed payment or contact the IRS before the agreement is canceled.

How does the IRS decide your monthly payment?

For Simple Payment Plans, the IRS usually lets you choose a payment that clears the balance in time. For larger or complex cases, it reviews Form 433 financial details, including your income, allowable living expenses, and assets, then sets a payment based on what you can afford.

Will an IRS installment agreement hurt your credit or passport?

The installment agreement itself does not appear on your credit report. A filed federal tax lien can, and it may affect loans or a mortgage. Passport problems usually only come up for seriously delinquent tax debt, a high balance threshold the IRS sets and adjusts each year.

Is an installment agreement easier to get than an Offer in Compromise?

Yes, by a wide margin. An installment agreement is approved for most taxpayers who can pay over time. An Offer in Compromise, which settles the debt for less, is much harder to win. The IRS accepted only about 14% of offers in fiscal year 2025.

Can self-employed people with irregular income qualify for a payment plan?

Yes. If your balance is within the Simple Payment Plan limit and you’re current on filing, you can usually set one up. The tricky part is choosing a payment you can keep during slow months, and remembering to budget for your current-year estimated taxes on top of it.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments