Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 24, 2026

Chapter 7 bankruptcy can wipe out credit card balances, medical bills, and personal loans in about four to six months. The trade-off is a 10-year mark on your credit report and the possible loss of non-exempt property. For most filers, the math works in their favor. But “most filers” isn’t everyone, and the difference matters.

The pros and cons of filing Chapter 7 bankruptcy depend almost entirely on your specific financial picture: what you owe, what you own, and how much you earn. I’ve worked with people who waited two years too long to file and people who filed when a different option would have saved them money. Both mistakes come from the same place: not understanding the actual trade-offs.

This article breaks down the real benefits, the real drawbacks, and the costs involved so you can make that call with actual numbers instead of fear.

What Is Chapter 7 Bankruptcy?

Chapter 7 is a federal bankruptcy filing that eliminates most unsecured debts by liquidating non-exempt assets. A court-appointed trustee reviews your finances, sells anything that isn’t protected by state or federal exemptions, and uses the proceeds to pay creditors. Whatever debt remains after that process gets discharged permanently.

Chapter 7 bankruptcy is a court-supervised process that erases qualifying debts (credit cards, medical bills, personal loans) in exchange for surrendering non-exempt assets, typically completing in four to six months with a 95% discharge success rate according to the American Bankruptcy Institute.

The word “liquidation” makes it sound like you’ll lose everything. That’s not how it plays out. Over 95% of Chapter 7 filers keep all their property because exemptions cover their belongings. The typical Chapter 7 case is what attorneys call a “no-asset case,” meaning the trustee finds nothing worth selling.

Consumer Chapter 7 filings hit 332,706 in 2025, a 15% jump from 2024 according to Epiq AACER data. That’s not a sign of economic collapse. It’s a sign that more people are choosing a structured reset over years of minimum payments going nowhere.

The Real Pros of Filing Chapter 7 Bankruptcy

The Automatic Stay Stops Collections Immediately

The second your Chapter 7 petition hits the court’s docket, a federal order called the “automatic stay” kicks in. Creditor calls stop. Collection letters stop. Wage garnishments stop. Pending lawsuits freeze. If a foreclosure sale is scheduled for next week, the automatic stay can halt that too.

This isn’t a polite request. It’s a court order with teeth. Creditors who violate the automatic stay can be forced to pay damages and attorney fees. I’ve seen clients go from fielding six collector calls a day to zero overnight. That alone is worth understanding, even if you never end up filing.

The stay protects you while the court processes your case. For most Chapter 7 filers, that’s roughly four to six months. Secured creditors (like your mortgage lender or auto loan company) can ask the court to lift the stay, but unsecured creditors almost never get that request granted.

Does Chapter 7 Actually Wipe Out All Your Debt?

Not all of it. But it eliminates most of the debt types that bury people.

Chapter 7 discharges credit card debt, medical bills, personal loans, old utility bills, and many other unsecured obligations. According to the National Consumer Law Center, the discharge also eliminates any deficiency balance after a foreclosure or repossession, which surprises a lot of people.

What it won’t erase: most tax debts, alimony, child support, student loans (with limited exceptions), and debts from fraud or DUI judgments. If tax debt is your primary burden, filing bankruptcy for IRS tax debt forgiveness might still be an option, but only if that debt meets specific age and filing requirements. Tax obligations less than three years old almost always survive bankruptcy.

Most Filers Get Their Debts Discharged

Here’s a stat that should settle some nerves: roughly 95% of Chapter 7 cases end in a successful discharge, according to the American Bankruptcy Institute. That’s not a coin flip. It’s close to a guarantee, provided you meet the eligibility requirements.

Those requirements aren’t complicated. You need to pass the means test, complete your bankruptcy forms accurately, take two required courses (credit counseling before filing and debtor education after), and respond to any requests from your assigned trustee. Skip the second course and your discharge won’t happen. That’s a mistake I’ve seen trip up otherwise simple cases.

Will You Lose Your Property in Chapter 7?

Probably not. Over 95% of Chapter 7 filers keep everything they own.

Every state has exemption laws that protect specific types of property from creditors. Your household furniture, clothing, and basic personal items are almost always exempt. Most states protect a vehicle up to a certain value (often $4,000-$7,500). Your retirement accounts are protected under federal law regardless of which state you live in.

If you’re paying on a car loan and want to keep the vehicle, you’ll need to stay current on payments. Can’t afford the car note anymore? You can surrender the vehicle and have the remaining loan balance discharged. Then find something more affordable.

The people most at risk of losing property in Chapter 7 are those with significant equity in real estate beyond their state’s homestead exemption, or those with luxury items, boats, or second properties. If that describes you, talk to a bankruptcy attorney before filing. The consultation is usually free.

You’ll Still Have Access to Credit After Filing

This is the part that confuses people the most. You’d expect lenders to avoid you after a bankruptcy. The opposite happens.

Within weeks of your discharge, you’ll likely receive credit card offers. Lenders know you can’t file Chapter 7 again for eight years, which makes you a safer bet than someone drowning in existing debt. The catch is that early offers come with high interest rates, sometimes 20-29%.

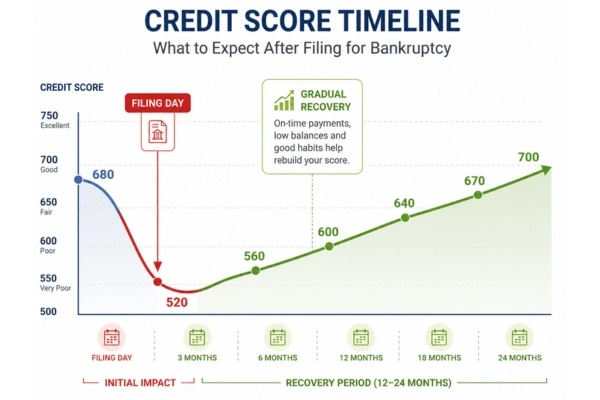

Based on FICO scoring models, a typical credit score drop falls between 130 and 240 points after a Chapter 7 filing. Someone starting at 750 might land around 550. Someone already at 550 from missed payments might barely notice a change. But here’s the part most articles skip: many filers see their credit score climb to 700 or above within 12-24 months of discharge, according to bankruptcy attorneys tracking client outcomes. The elimination of all those negative debt balances resets your debt-to-income ratio to nearly zero, and that’s a powerful signal to scoring algorithms.

A secured credit card with on-time payments is the fastest rebuild tool. Don’t take every offer that shows up.

What Are the Cons of Filing Chapter 7?

Not Everyone Qualifies for Chapter 7

You have to pass the means test, which compares your household income to the median income in your state. If you earn more than the median, you’ll need to show that after allowed deductions (housing, transportation, childcare, medical), you don’t have enough disposable income to fund a repayment plan.

Fail the means test and you’re looking at Chapter 13 instead, which requires a three-to-five-year repayment plan. Chapter 13 offers its own advantages (especially for keeping property with non-exempt equity), but it’s slower, more expensive, and more complex. If tax debt is part of the equation, understanding how bankruptcy affects your tax relief options matters before you commit to either chapter.

How Bad Is the Credit Score Damage?

It’s real, but it’s not permanent, and it’s not as catastrophic as the internet makes it sound.

Chapter 7 stays on your credit report for 10 years from the filing date. That’s three years longer than most negative items like collections or late payments. Based on FICO scoring models, the initial drop ranges from 130 to 240 points, with higher starting scores taking bigger hits.

| Starting Score | Typical Drop | Post-Filing Range |

| 750+ | 150-240 points | 510-600 |

| 650-749 | 130-180 points | 470-620 |

| Below 650 | 50-130 points | 400-600 |

The real question isn’t “how much will my score drop?” It’s “how does that compare to where I’ll be in two years if I don’t file?” Someone making minimum payments on $40,000 in credit card debt at 24% interest will spend years treading water while their score stays depressed from high utilization. Filing Chapter 7 resets that clock.

Some Debts Won’t Go Away

Chapter 7 can’t touch these:

- Child support and alimony

- Most student loans (unless you prove “undue hardship,” which became slightly easier after the Department of Justice issued updated guidelines in late 2022)

- Recent tax debts (generally less than three years old)

- Debts from fraud, embezzlement, or willful injury

- Government fines and penalties

- DUI-related judgments

If most of your debt falls into these categories, Chapter 7 won’t solve your problem. For tax debt specifically, other resolution options like an offer in compromise or installment agreement might be better paths.

You Could Lose Non-Exempt Property

This is the risk everyone fixates on, but it affects very few filers. The trustee assigned to your case reviews your assets and compares them against your state’s exemption limits. Anything with equity beyond those limits can be sold.

In practice, it’s rare. Most people filing Chapter 7 don’t own valuable unprotected assets. If you do own something with significant non-exempt equity (say, a paid-off second car worth $15,000 in a state with a $5,000 vehicle exemption), you should know about it before you file.

A bankruptcy attorney can tell you in one meeting whether any of your property is at risk. That’s why the free consultation exists.

Your Co-Signers Don’t Get Protection

This is the con people don’t think about until it’s too late. Chapter 7 eliminates your obligation to pay a debt. It doesn’t eliminate the debt itself. If your parent co-signed a car loan with you and you file Chapter 7, the lender can go after your parent for the full balance.

Chapter 13 offers a “co-debtor stay” that protects co-signers while you’re making plan payments. Chapter 7 doesn’t have that. If someone you care about is on the hook for your debt, factor that into your decision.

How Much Does Chapter 7 Bankruptcy Cost in 2026?

The court filing fee is $338, set at the federal level and the same in every district. That covers a $245 filing fee, a $78 administrative fee, and a $15 trustee surcharge. If your household income falls below 150% of the federal poverty guidelines (roughly $23,940 for a single filer in 2026), you can apply for a full fee waiver.

Attorney fees are the biggest cost. Expect to pay $1,500 to $2,500 for a standard case in a mid-size city according to Nolo’s 2026 bankruptcy cost guide, though complex cases or expensive markets can push that past $3,000. Many attorneys offer payment plans, and some let you redirect money you’d normally send to creditors toward the legal fee once you’ve decided to file.

You’ll also need two required courses: a credit counseling session before filing and a debtor education course after. Each costs $50 or less, and both can be done online.

| Cost Item | Amount |

| Court filing fee (uscourts.gov) | $338 |

| Attorney fees (Nolo, 2026) | $1,500-$2,500 |

| Credit counseling course | $15-$50 |

| Debtor education course | $15-$50 |

| Estimated total | $1,870-$2,940 |

Compare that to what you’d pay in interest over the next three years on $30,000 in credit card debt. Bankruptcy is cheaper. For people dealing with tax problems alongside consumer debt, the cost analysis gets even more lopsided because unresolved obligations compound with penalties and interest every month you wait.

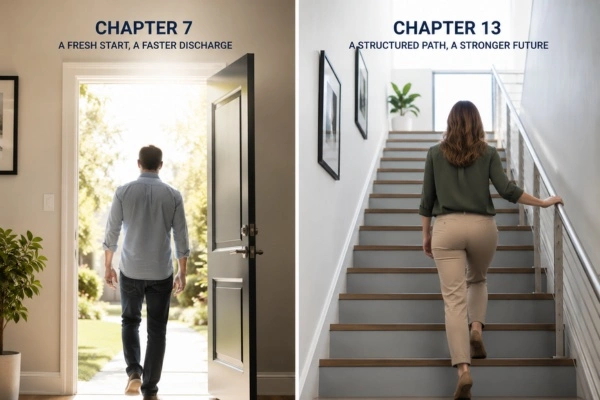

Chapter 7 vs. Chapter 13 – Which One Fits?

| Factor | Chapter 7 | Chapter 13 |

| Timeline | 4-6 months | 3-5 years |

| Income requirement | Below state median (means test) | Regular income required |

| Property risk | Non-exempt assets can be sold | You keep property but repay through plan |

| Debt discharge | Immediate after case closes | After completing repayment plan |

| Credit report impact | 10 years | 7 years |

| Co-signer protection | None | Co-debtor stay available |

| Cost (estimated) | $1,870-$2,940 | $3,300-$5,500 |

| Best for | Low-income filers with mostly unsecured debt | Higher earners who want to keep non-exempt assets |

Chapter 13 is more complex and almost always requires an attorney. It’s the better choice when you have significant non-exempt property to protect or when you’re behind on a mortgage and need time to catch up. For everyone else, Chapter 7 is faster, cheaper, and just as effective at eliminating unsecured debt.

FAQs

How long does Chapter 7 bankruptcy take from start to finish?

Most Chapter 7 cases wrap up in four to six months. You’ll file your petition, attend one meeting with the trustee (called the 341 meeting, usually lasting under 10 minutes), and receive your discharge order roughly 60-90 days later. Cases with complications like contested assets or creditor objections can take longer.

Will filing Chapter 7 bankruptcy stop the IRS from collecting tax debt?

The automatic stay temporarily halts IRS collection activity, including wage levies and bank account seizures. But most tax debts survive Chapter 7 unless they meet strict requirements: the tax return was due at least three years ago, it was filed at least two years ago, and the IRS assessed the tax at least 240 days before your bankruptcy filing. Tax debts that don’t meet all three conditions won’t be discharged.

Can I keep my house if I file Chapter 7?

Yes, as long as you’re current on your mortgage payments and the equity in your home doesn’t exceed your state’s homestead exemption. Michigan’s homestead exemption protects a set amount of home equity that adjusts periodically, so check the current figure with a bankruptcy attorney. If your equity exceeds the exemption, the trustee could force a sale. Over 95% of Chapter 7 filers keep their homes, according to American Bankruptcy Institute data.

How much does Chapter 7 bankruptcy cost in 2026?

The federal court filing fee is $338, and attorney fees typically range from $1,500 to $2,500 for a standard case according to Nolo. You’ll also pay under $50 each for two required courses (credit counseling and debtor education). Total estimated cost for most filers lands between $1,870 and $2,940. Fee waivers are available if your income is below 150% of the federal poverty guidelines.

Does Chapter 7 discharge student loan debt?

It can, but only if you prove “undue hardship” through a separate court proceeding called an adversary complaint. The Department of Justice updated its guidance in late 2022 to make these cases slightly easier, but the bar remains high. Private student loans may be easier to discharge than federal ones depending on the loan terms.

How soon can I rebuild my credit after Chapter 7?

Rebuilding starts immediately after discharge. Bankruptcy attorneys report that many filers gain 100-150 points within 6-12 months by opening a secured credit card and making on-time payments. Reaching a 700+ score within 12-24 months is realistic for people who manage new credit carefully. The bankruptcy stays on your report for 10 years, but its scoring impact fades significantly after the first two years.

Can I file Chapter 7 more than once?

You can file again, but not right away. Federal law requires an eight-year gap between Chapter 7 discharge dates. If you received a Chapter 13 discharge, you’ll need to wait six years before filing Chapter 7 (unless you paid at least 70% of unsecured debts in your Chapter 13 plan, which reduces the wait to four years).

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments