You don’t need a complicated financial plan to lower your taxes. Most people overpay because they don’t act until April, and by then, the best moves are off the table. The eight strategies below work for W-2 employees, self-employed filers, and retirees. Some take five minutes. Others need a conversation with a tax professional. But every one of them can put real money back in your pocket if you use them before December 31.

The most effective ways to lower your taxes in 2026 include maximizing retirement account contributions, funding a health savings account, claiming all eligible tax credits, and using strategies like tax-loss harvesting. Under the One Big Beautiful Bill Act signed in July 2025, several deductions and credits expanded or became permanent, giving filers more options than they’ve had in years.

This article won’t cover estate planning, trust strategies, or business entity restructuring. Those deserve their own deep treatment. What we’re covering here are the moves almost anyone can make before filing their 2026 return.

1. Why Year-Round Tax Planning Beats a Last-Minute Scramble

Tax planning done in January gives you 12 months of flexibility. Tax planning done in December gives you panic. I’ve seen clients leave $3,000–10,000 on the table simply because they didn’t check their withholding until it was too late to adjust.

Start the year by estimating your tax bracket. If your income straddles the line between the 22% and 24% brackets, even a small pre-tax contribution can knock you into the lower tier. By November, review where you stand again. You may find room to accelerate deductions or defer income, but only if you’ve been tracking all year. According to the NATP 2025 Fee Study, professional tax planning routinely yields 3–10x its cost through identified deductions and credits. That’s not a theoretical number. It’s what practitioners report seeing across real client portfolios.

2. How Do Retirement Contributions Lower Your Taxes?

Every dollar you put into a traditional 401(k) or traditional IRA reduces your taxable income by that same dollar. It’s the most direct way to reduce your taxes for the current year.

For 2026, 401(k) contribution limits sit at $23,500 ($31,000 if you’re 50 or older). Traditional IRA limits are $7,000 ($8,000 for 50+). If you’re a W-2 employee earning $85,000 and you max out your 401(k), you’ve just dropped your taxable income to $61,500. That’s a bracket shift for a lot of people.

Roth accounts work differently. Contributions don’t lower this year’s bill, but qualified withdrawals in retirement come out tax-free. If you think your future tax rate will be higher, Roth makes sense. If you need the deduction now, go traditional. Most people benefit from having both.

3. The HSA Triple Tax Advantage Most People Ignore

If you’re enrolled in a high-deductible health plan, a health savings account is the single most tax-efficient account available. Contributions reduce your taxable income today. Growth is tax-deferred. Distributions for qualified medical expenses are tax-free. No other account in the tax code offers all three.

For 2026, the HSA contribution limit is $4,300 for individuals and $8,550 for families. The contrarian take here: don’t spend your HSA on current medical bills if you can afford to pay out of pocket. Let the account grow for decades and you’ve built a tax-free medical fund for retirement. That strategy alone can be worth thousands over time.

4. What Is a Qualified Charitable Distribution?

A qualified charitable distribution (QCD) lets anyone 70½ or older donate up to $105,000 directly from an IRA to a qualified charity. The distribution doesn’t count as taxable income, and it can satisfy your required minimum distribution (RMD) if you have one.

Here’s why this matters more than a regular charitable deduction. A standard deduction filer gets zero tax benefit from writing a check to charity. A QCD bypasses that entirely because the money never hits your adjusted gross income. It works whether you itemize or not. If you’re charitably inclined and over 70½, skipping this strategy is leaving money on the table.

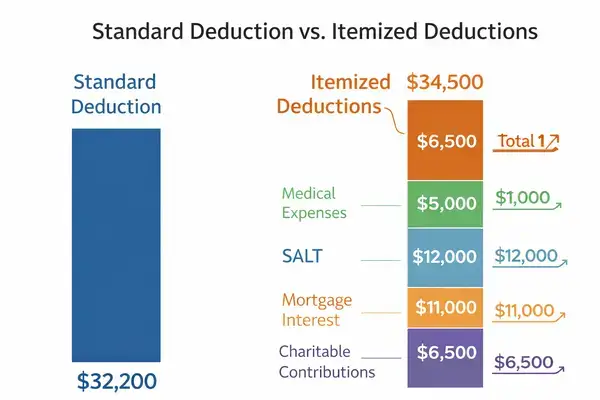

5. Should You Itemize or Take the Standard Deduction in 2026?

The standard deduction for 2026 is $32,200 for married couples filing jointly and $16,100 for single filers, per IRS inflation adjustments incorporating the OBBBA. Under the new law, the SALT deduction cap jumped from $10,000 to $40,000 (phasing down above $500,000 AGI). That’s a big deal for filers in high-tax states.

If you’re itemizing, the biggest wins come from mortgage interest, qualified charitable gifts, and unreimbursed medical expenses that exceed 7.5% of AGI. One strategy worth considering: “bunching” deductions. Push two years of charitable giving into a single year, itemize that year, and take the standard deduction the next. It’s the same total giving, but the tax benefit is significantly larger.

Actually, a better way to think about bunching is this. Run the math both ways every single year. Most people default to one or the other and never check. A good tax professional will model both scenarios for you, and the difference often surprises people.

6. Tax Credits Hit Harder Than Deductions

A tax deduction reduces your taxable income. A tax credit reduces your actual tax bill, dollar for dollar. If you’re in the 22% bracket, a $1,000 deduction saves you $220. A $1,000 credit saves you the full $1,000. Credits are more valuable, and most filers don’t claim everything they’re entitled to.

The OBBBA introduced and expanded several credits for 2026, including larger employer-provided childcare credits and new deductions for tips (up to $25,000) and overtime income (up to $12,500 single / $25,000 joint). Review the full list of OBBBA tax provisions with your tax advisor. The difference between tax credits and tax relief programs matters, and understanding that distinction could save you thousands.

7. How Tax-Loss Harvesting Turns Losses Into Savings

Tax-loss harvesting means selling investments that have dropped in value to offset capital gains from winners. If you realized $10,000 in gains and $7,000 in losses, you only owe taxes on $3,000 of net gains. If your losses exceed your gains, you can deduct up to $3,000 against ordinary income and carry the rest forward.

The catch: the IRS wash-sale rule prevents you from buying a “substantially identical” security within 30 days before or after the sale. You can buy something similar (a different index fund tracking the same sector, for example) but not the exact same holding. This strategy works best in taxable brokerage accounts, not retirement accounts. If your portfolio took hits this year, work with someone who understands how tax relief works to make sure you execute it properly.

8. Tax-Gains Harvesting: The Move Nobody Talks About

This is the reverse of tax-loss harvesting, and it’s wildly underused. If you’re in a year where your income is unusually low (maybe you took time off, changed careers, or retired mid-year), you might fall into the 0% long-term capital gains bracket. For 2026, that bracket applies to single filers with taxable income under roughly $48,350 and married couples under roughly $96,700.

In a low-income year, you can sell appreciated investments and pay zero federal tax on the gains. You’ve now reset your cost basis higher, which means less tax when you eventually sell for real. I’ve seen this save clients anywhere from $2,000 to $15,000 in a single year. It takes planning and precise timing, so don’t wing it.

The real difference between people who overpay taxes and people who don’t isn’t income level. It’s planning. Start early, run the numbers quarterly, and don’t assume last year’s strategy still works. The tax code changed significantly in 2025, and the filers who adjust will keep more of what they earn. If you’re not sure where to start, a digital marketing team can help you find what you’re missing.

FAQs

What is the fastest way to lower your taxes in 2026?

The fastest move is increasing pre-tax retirement contributions. Every dollar contributed to a traditional 401(k) or IRA directly reduces your taxable income. For 2026, you can contribute up to $23,500 to a 401(k) ($31,000 if 50+). If you’re self-employed, a SEP-IRA allows contributions up to 25% of net earnings.

How much can a tax professional save me compared to DIY filing?

According to the NATP 2025 Fee Study, professional tax planning typically yields 3–10x its cost in identified deductions and credits. Professional fees range from $280 for a basic 1040 (CPA) to $1,000–$5,000+ for complex returns, but they routinely find $2,000–$20,000 in savings that software misses.

Does the One Big Beautiful Bill Act change how I file in 2026?

Yes. The OBBBA, signed July 4, 2025, permanently extended the higher standard deduction ($32,200 for joint filers in 2026), raised the SALT cap to $40,000, made the 20% QBI deduction permanent, restored 100% bonus depreciation, and introduced new deductions for tips and overtime income. These changes affect both itemizers and standard deduction filers.

Is the home office deduction safe to claim in 2026?

Yes, if you’re self-employed and use a dedicated space regularly and exclusively for business. The myth that this deduction triggers audits is outdated. With proper documentation (square footage, expenses, photos), it’s one of the safest deductions available. W-2 employees don’t qualify under current law.

What is the difference between a tax credit and a tax deduction?

A deduction reduces your taxable income. A credit reduces your actual tax bill dollar for dollar. In the 22% bracket, a $1,000 deduction saves $220, while a $1,000 credit saves the full $1,000. Credits are almost always more valuable, and many filers miss credits they qualify for.

Can I lower my taxes by investing in an HSA?

An HSA is the only account with a triple tax benefit: contributions lower taxable income, growth is tax-deferred, and distributions for medical expenses are tax-free. For 2026, contribution limits are $4,300 (individual) and $8,550 (family). You must be enrolled in a high-deductible health plan to qualify.

What questions should I ask before hiring a tax professional?

Ask about their audit defense policy, their track record with IRS appeals, how they stay current on tax law changes like the OBBBA, and whether they proactively plan or just prepare returns. A good professional identifies savings year-round, not just during filing season. The NATP reports that nearly half of all professionals price by complexity, so get a clear fee estimate upfront.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments