Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 18, 2026

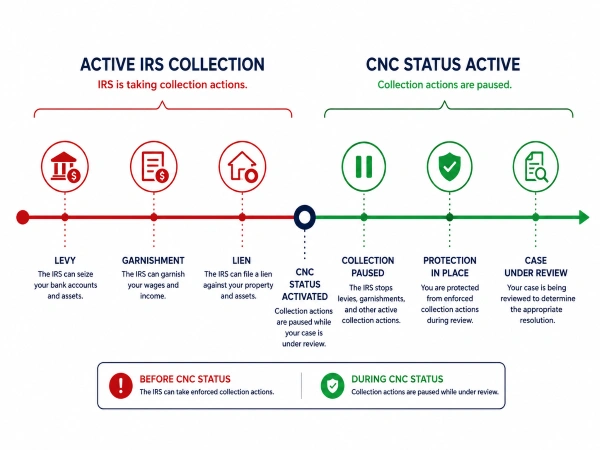

You can stop IRS wage garnishments, bank levies, and property seizures by getting your account placed in currently not collectible (CNC) status. It costs nothing to apply. You call the IRS, submit a two-page form proving you can’t cover basic living expenses and pay your tax debt at the same time, and the IRS pauses all active collection. Most people who qualify for CNC don’t need to pay a professional to do it for them, but the tax relief industry has built a business model around charging thousands of dollars for what’s often a single phone call plus paperwork.

IRS currently not collectible status is a temporary hold on collection activity granted when a taxpayer proves that paying any amount toward their tax debt would prevent them from meeting basic living expenses like rent, food, utilities, and medical care. CNC doesn’t erase what you owe. It pauses the pressure.

This article won’t cover offers in compromise or installment agreements in depth. Those are different programs for different situations. We’re focused on CNC: who qualifies, how to prove hardship, and what actually happens after you get it.

What Currently Not Collectible Status Really Means

When the IRS classifies your account as CNC, it stops levies, garnishments, and asset seizures. That’s the upside. The trade-offs are real, though.

The IRS will still grab your tax refund every year and apply it to your balance. If you owe more than $10,000, it’ll probably file a Notice of Federal Tax Lien against you, which shows up on your credit report. And penalties plus interest keep piling up the entire time you’re in CNC.

So CNC is a pause button, not a delete button. You still owe the full amount. The IRS just agrees to stop chasing it for now.

Does CNC Last Forever?

For most people, no. The IRS runs an annual review of your income using W-2 and 1099 data reported by your employers and clients. If your earnings cross a certain threshold tied to your assigned “closing code” (codes 24–32 under IRS Internal Revenue Manual 5.16.1, revised March 2025), the IRS will reactivate collection.

But there’s a scenario where CNC does become permanent. The IRS has a 10-year statute of limitations to collect any assessed tax debt. This is called the collection statute expiration date (CSED). If your income never improves enough to trigger reactivation, and the CSED expires while you’re still in CNC, the IRS writes off the debt entirely. For someone on permanent disability or a fixed retirement income, this is often the best outcome available.

Ask the IRS which closing code they’ve assigned to your account. That number tells you exactly what income level triggers a review. If you’ve been assigned a revenue officer, ask them directly. If not, call the number on your most recent notice.

When Your Income Improves, the IRS Comes Back

The IRS doesn’t need you to tell them your income went up. Every W-2 and 1099 filed by anyone who pays you goes straight to them. If your earnings cross your closing code threshold, you’ll get a letter saying collection activity is restarting.

At that point, you’d need to explore other options. Many taxpayers move into a monthly installment agreement or a partial payment plan. Life changes like adding a dependent could also keep you in CNC despite higher income, so it’s worth running the numbers before you assume you’ve lost the status.

If you know your financial situation will improve within the next year or two, CNC might not be your strongest play. You’d want to look at other resolution options that actually reduce what you owe rather than just delay it.

When the IRS Agrees to Grant CNC Status

The IRS doesn’t hand out CNC status because you’re having a tough month. You have to prove that making any payment toward your tax debt, even $25, would keep you from affording rent, groceries, utilities, or medical care. That bar is specific and documented.

CNC also isn’t automatic. You apply, submit financial proof, and wait for the IRS to compare your income against their standardized expense limits. If you can afford even a small monthly payment, the IRS will push you toward a partial payment installment agreement (PPIA) instead. That’s a different program entirely.

One update worth knowing: the IRS now accepts digital uploads of Form 433-F through an online correspondence portal, which has sped up processing compared to the old mail-only system. The IRS also updates its Collection Financial Standards annually to reflect current costs of living, which affects how much disposable income the IRS calculates you have.

Here are four situations where the IRS commonly grants CNC.

The 10-Year Collection Deadline Is Almost Up

The IRS gets 10 years from the assessment date to collect. If only a year or two remains on that clock and you genuinely can’t pay without going hungry, the IRS often agrees to CNC. Starting a payment plan with 18 months left on the statute rarely makes sense for either side.

Government Benefits Are Your Only Income Source

If you live entirely on Social Security, disability benefits, SNAP, or public housing assistance, you likely have zero disposable income. The IRS knows this. These cases are among the most straightforward CNC approvals because there’s simply nothing left after covering the basics a tax professional would walk you through.

CNC isn’t guaranteed to stick forever, though. If you start earning other income, the IRS will review your case.

You’re Unemployed and Collecting Benefits

Job loss creates an immediate income gap. If unemployment compensation is all you’ve got, and using it to pay back taxes would mean missing rent or skipping meals, the IRS will usually agree this isn’t the right time to collect.

Another Financial Hardship Blocks Any Payment

Serious illness, disability, caregiving costs, or a sudden income drop all qualify. The IRS will ask for documentation. Bank statements, pay stubs, medical bills, proof of expenses. They want to confirm that even a small monthly payment would cause real problems, not just inconvenience.

How Do You Prove Financial Hardship to the IRS?

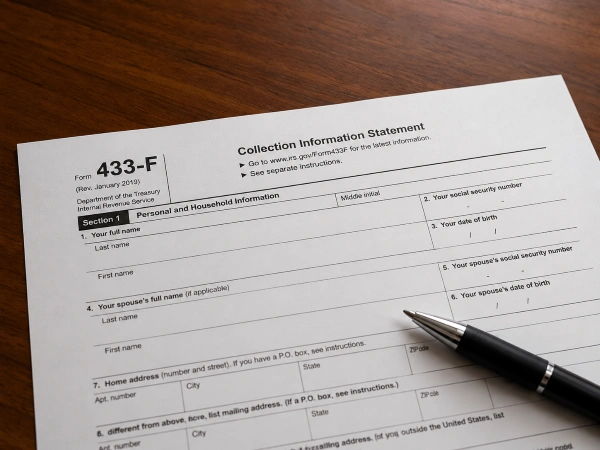

You prove it with IRS Form 433-F (Collection Information Statement). It’s two pages. You list your monthly income, expenses, debts, and assets. Then you attach supporting documents: pay stubs, bank statements, utility bills, rent or mortgage statements, and medical expense receipts.

One thing most people don’t realize: you must be current on all tax return filings before the IRS will even consider CNC. If you have unfiled returns, those need to go in first. The IRS won’t grant you a break on old debt while you’re not filing new returns.

The IRS compares your reported income against your allowable expenses. If there’s nothing left over, CNC gets approved. If even $50/month is left, they’ll push for a payment arrangement.

Here’s the contrarian take most articles won’t give you: the single most expensive mistake in CNC cases is paying a high-fee tax relief company for a case you could handle yourself. If your situation is simple (single income source, standard expenses, no business assets), you probably don’t need to pay anyone. CNC-specific professional representation typically runs roughly $1,500–$3,500 based on published rate surveys from 2025–2026. For a case that amounts to one phone call and a two-page form, that’s hard to justify.

What Does the IRS Consider an Allowable Expense?

The IRS doesn’t use your actual spending. It applies standardized expense limits that vary by category and location.

- National standards set maximums for food, clothing, and out-of-pocket health costs

- Local standards (based on your county and household size) cap housing, utilities, and transportation

- Other approved expenses include health insurance, court-ordered payments, childcare, and life insurance

These IRS Collection Financial Standards are updated annually to keep pace with cost-of-living shifts. That annual adjustment actually helps CNC applicants because higher allowable expenses mean less “disposable income” on paper.

If your income after these standardized deductions can’t support any payment at all, CNC approval is likely.

CNC vs. Other IRS Relief Options (IRS-Published Costs Only)

| CNC Status | Installment Agreement | Offer in Compromise | |

| IRS Application Fee | $0 | $22–$178 setup (per TAS, March 2026) | $205 (waivable for low income) |

| Reduces Debt? | No (penalties/interest accrue) | No (pay full amount over time) | Yes (settle for less than owed) |

| Stops Levies? | Yes | Yes | Yes (during review) |

| Best For | Can’t pay anything right now | Can afford monthly payments | Can pay a lump sum less than full balance |

The Single Factor That Decides Your Next Step

If you can’t pay a single dollar toward your tax debt without missing rent or going without food, currently not collectible status is the right move. Don’t overthink it. Call the IRS at 800-829-1040, request CNC, complete Form 433-F with accurate numbers, and submit your supporting documents through the IRS collection delay process.

If you can afford something each month but not the full balance, a partial payment installment agreement or offer in compromise is a better path. And if your situation is complex (business assets, multiple tax years, revenue officer involvement), working with a tax resolution team who charges fair, transparent fees is worth the investment. The people who get burned are the ones who pay premium prices for a basic CNC case that doesn’t require professional help.

FAQs

Does CNC status forgive my tax debt?

No. CNC pauses IRS collection activity, but you still owe the full balance. Penalties and interest keep accruing, and the IRS will offset your future tax refunds against the debt. The only way CNC leads to debt elimination is if the 10-year collection statute (CSED) expires before your finances recover.

How long does currently not collectible status last?

There’s no fixed expiration. CNC lasts until your financial situation improves enough to trigger the closing code assigned to your account (codes 24–32 per IRM 5.16.1). The IRS checks your income annually through W-2 and 1099 data. If nothing changes and the 10-year CSED expires, the debt goes away.

Can I apply for CNC status online?

You start by calling the IRS at 800-829-1040. The IRS now accepts digital uploads of Form 433-F through its online correspondence portal, which speeds up the process compared to mailing documents. You can’t complete the full application online yet, but the paperwork submission portion is digital.

Will CNC stop an IRS tax levy or lien?

CNC stops active levies on your bank accounts and wages. A tax lien is different. If you owe $10,000 or more, the IRS will often file a Notice of Federal Tax Lien even after granting CNC status. That lien stays on your record until the debt is paid, the CSED expires, or you negotiate removal.

Do I need to file all my tax returns before getting CNC?

Yes. The IRS requires you to be current on all return filings before it will place your account in CNC. If you have unfiled returns from prior years, submit those first. The IRS won’t grant you a collection pause while you’re not meeting basic filing obligations.

How much does it cost to get CNC status on my own?

Zero. There’s no IRS application fee for CNC. You call 800-829-1040, submit Form 433-F with supporting documents, and the IRS makes a determination. The only costs are your time and effort gathering paperwork.

What happens if the IRS denies my CNC request?

The IRS usually suggests an installment agreement as an alternative. You can reapply with better documentation, reclassify expenses more accurately using IRS Collection Financial Standards, or appeal the decision. Denial often happens because of incomplete Form 433-F paperwork or unfiled prior-year returns, not because the taxpayer didn’t qualify.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments