Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 22, 2026

An IRS revenue officer is a federal employee who collects unpaid taxes that the IRS couldn’t resolve through automated systems. If one has been assigned to your case, it means the IRS considers your tax debt a high priority. Revenue officers can file federal tax liens, levy bank accounts, garnish wages, and (in rare cases) seize property. The single most important thing you can do right now is respond promptly and work with a qualified tax resolution team before your first meeting.

An IRS revenue officer is a field collection employee within the IRS Small Business/Self-Employed (SB/SE) Division, assigned to resolve tax debts that the Automated Collection System (ACS) failed to collect. Revenue officers handle face-to-face contact with taxpayers and carry broader enforcement authority than ACS representatives, including the ability to file liens, issue levies, and recommend settlement agreements.

Most taxpayers never deal with a revenue officer. The IRS reserves field collection for cases it can’t close by phone or mail. So if you’ve received that letter or business card, your case has been flagged as one that requires personal attention. That’s not a death sentence, but it’s not something you can sit on either.

Why Would an IRS Revenue Officer Be Assigned to Your Case?

Revenue officers don’t get assigned randomly. The IRS spends real money putting people in the field, so they’re selective about it.

Your case likely landed on a revenue officer’s desk for one of these reasons:

- Your individual tax balance exceeds roughly $100,000 (thresholds vary by region, but this is the common benchmark from multiple practitioner sources).

- ACS already tried to collect and failed. Maybe you ignored notices, missed installment payments, or the automated system just couldn’t reach a resolution.

- You haven’t filed tax returns for multiple years. The IRS treats non-filing as a compliance issue that requires in-person follow-up, even if you don’t owe much.

- You’re a business with unpaid payroll tax deposits. This is the IRS’s top collection priority. Payroll tax cases almost always get a revenue officer, regardless of the dollar amount.

- The IRS believes collection may be at risk. If there’s any sign you’re moving assets or preparing to leave the country, the case gets fast-tracked.

I’ve seen cases assigned to revenue officers for balances as low as $40,000 when the taxpayer had years of unfiled returns stacked on top. It’s not always about the dollar amount. It’s about the IRS’s perception of risk.

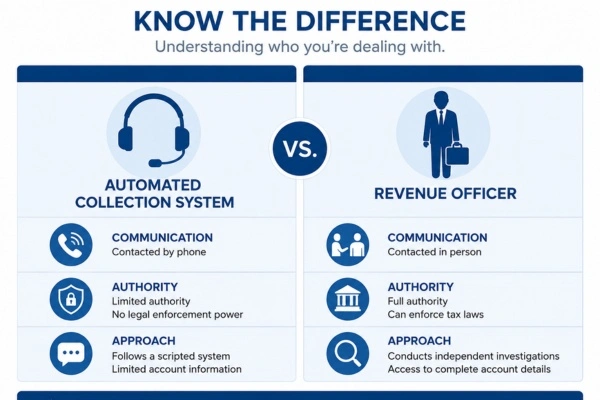

How Is a Revenue Officer Different from an ACS Agent?

This is where most people get confused. ACS agents work in call centers. They follow scripts, process installment agreements, and handle the bulk of IRS collection work. A revenue officer is a different animal entirely.

Revenue officers work in the field. They can show up at your home or business (though surprise visits are less common than people think). They carry IRS-issued credentials, and they have authority that ACS agents don’t. According to a 2025 TIGTA report, revenue officers initiate most levies, not the automated system.

Here’s what a revenue officer can actually do:

- File a Notice of Federal Tax Lien (NFTL) against your property. This becomes a public record and can damage your credit score significantly. Industry estimates suggest a drop of 100+ points isn’t unusual.

- Issue levies on bank accounts using Form 668-A. A bank levy freezes your entire balance (not a portion) and holds it for 21 days before the IRS takes it permanently.

- Garnish wages using Form 668-W, taking a portion of every paycheck until the debt is satisfied.

- Seize physical assets like vehicles, equipment, or real estate. This is rare and usually requires management approval, but it happens in cases with large balances and zero cooperation.

A revenue officer can also negotiate on your behalf toward a resolution. That’s the part most articles leave out. Their job isn’t just enforcement. They’re authorized to set up installment agreements, recommend offer in compromise acceptance, place accounts in Currently Not Collectible (CNC) status, and work out partial-pay arrangements.

What Does the Revenue Officer Meeting Actually Look Like?

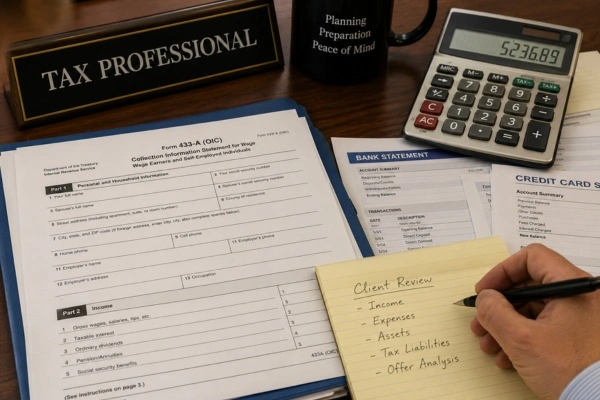

Once a revenue officer is assigned, they’ll contact you (usually by mail, sometimes by phone) to schedule a meeting. At that meeting, they’ll ask you to complete a Collection Information Statement (Form 433-A for individuals, Form 433-B for businesses, or Form 433-F for simpler cases).

This form asks for everything. Bank accounts, investments, real estate, vehicles, credit card balances, monthly living expenses, employment details. They’ll also want supporting documents: three months of bank statements, pay stubs, mortgage statements, and proof of monthly expenses.

The revenue officer uses this information to calculate your “reasonable collection potential,” which is essentially what the IRS believes you can afford to pay. If full payment isn’t realistic, they’ll explore alternatives. But here’s the catch: how you present your financial picture matters enormously. The IRS uses its own Collection Financial Standards to determine allowable expenses, and you have specific rights as a taxpayer throughout this process. If you don’t know those standards or those rights, you might accept a payment plan that’s far higher than it needs to be.

What Should You Avoid Saying to a Revenue Officer?

This is where I’ll push back on something most firms repeat without thinking. You’ll see advice everywhere saying “be cooperative and honest.” And yes, you should be cooperative. But “cooperative” doesn’t mean volunteering information they haven’t asked for.

Revenue officers are trained investigators. Anything you say can and will be used to assess your ability to pay. Mentioning a side income stream, a recent inheritance, or even a planned vacation can change the math on your case. I’ve seen taxpayers accidentally bump their own payment plan up by thousands of dollars because they mentioned a rental property during casual conversation.

Don’t meet or speak with a revenue officer without representation. Period. A qualified tax professional can negotiate directly with the IRS on your behalf using Form 2848 (Power of Attorney). Once that form is filed, the revenue officer communicates with your representative, not you. This isn’t about hiding anything. It’s about making sure every word spoken moves your case toward the best possible outcome.

Do Business Owners Face Different Rules?

Yes, and it’s worse than most business owners realize.

If your business owes payroll taxes (the money withheld from employee paychecks for Social Security and Medicare), the IRS assigns a revenue officer regardless of the balance. Payroll tax cases are the IRS’s number-one enforcement priority, and even relatively small balances can trigger field collection assignment. Whether you’re a sole proprietor or running a larger operation, business taxpayers face a different set of risks than individuals do.

On top of that, the IRS can assess a Trust Fund Recovery Penalty (TFRP) against the individuals responsible for withholding and depositing payroll taxes. That means you’re personally liable for the unpaid amount, even if your business is an LLC or corporation. In 2024, over 3.8 million taxpayers were subject to IRS collection actions including liens and levies, according to IRS enforcement data reviewed by the Treasury Inspector General for Tax Administration. A disproportionate share of those involved business taxpayers with payroll issues.

How Can Austin & Larson Tax Resolution Help?

Revenue officer cases aren’t something you want to handle alone. The stakes are too high, and the margin for error is too small. Revenue officers juggle up to 50 cases at a time. They want to close your file quickly. If you don’t have a clear strategy walking in, you’ll end up with whatever resolution is easiest for them, not what’s best for you.

At Austin & Larson Tax Resolution, we deal with revenue officer cases regularly. We file Form 2848 so the revenue officer talks to us, not you. We prepare your Collection Information Statement using the IRS’s own financial standards to make sure your allowable expenses are maximized. And we push for the resolution that actually fits your situation, whether that’s an installment agreement, an offer in compromise, Currently Not Collectible status, or penalty relief.

If you’ve received a letter from a revenue officer, or you suspect one may be assigned to your case, reach out for a consultation before that first meeting happens. Getting representation early is the single biggest factor in how these cases turn out.

FAQs

Can an IRS revenue officer show up at your home without warning?

Yes, but it’s uncommon. Revenue officers can make unannounced visits to your home or business, though they typically mail a letter or leave a business card first. If someone claims to be from the IRS and shows up at your door, ask for their credentials and HSPD-12 card. You can verify their identity by calling the IRS at 1-800-829-1040.

How long do you have to respond to an IRS revenue officer?

Revenue officers typically set a deadline of 10 to 30 days in their initial contact letter. Missing that deadline doesn’t trigger immediate enforcement, but it signals non-cooperation, which speeds up lien and levy actions. In most cases, the IRS must wait 30 days after sending a Final Notice of Intent to Levy before seizing assets.

What’s the difference between a revenue officer and a revenue agent?

A revenue officer collects unpaid taxes. A revenue agent audits tax returns. They work in different IRS divisions. Revenue officers fall under SB/SE Collection, while revenue agents work in the Examination division. If you’re dealing with an unpaid balance, you have a revenue officer. If the IRS is questioning your deductions or income, that’s a revenue agent.

Can an IRS revenue officer put you in jail?

No. Revenue officers handle civil collection only. They can’t arrest you or refer your case for criminal prosecution on their own. Criminal tax cases are handled by IRS Criminal Investigation (IRS-CI) special agents, who carry firearms and have law enforcement authority. Revenue officers are unarmed civilian employees.

What happens if you ignore an IRS revenue officer?

Ignoring a revenue officer is one of the fastest ways to trigger enforcement. They can file a federal tax lien (which becomes a public record and damages your credit), levy your bank accounts (freezing the full balance for 21 days), garnish your wages, and in extreme cases seize physical assets. In 2024, over 3.8 million taxpayers faced IRS collection actions, and cases assigned to revenue officers tend to see faster enforcement timelines.

Does hiring a tax professional stop the IRS revenue officer from contacting you?

Yes. Once your representative files Form 2848 (Power of Attorney and Declaration of Representative), the revenue officer must direct all communication to your representative. This is a legal right under the IRS Restructuring and Reform Act. You don’t have to speak with the revenue officer again unless you choose to.

How much tax debt triggers an IRS revenue officer assignment?

There’s no hard-and-fast rule, but individual balances over $100,000 are the most common threshold for revenue officer assignment. Business cases with unpaid payroll taxes can get assigned at much lower amounts. Non-filing (having multiple years of unfiled returns) can also trigger assignment regardless of the balance owed.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments