A tax audit is the IRS reviewing your return to confirm you reported everything correctly and paid the right amount. If you’ve never been through one, the word “audit” probably sounds worse than it is. But if you have been through one, you know it can cost real money and real time.

Roughly 0.20% of individual returns got examined in FY 2024, according to the IRS Data Book. That’s about 2 out of every 1,000 returns. Your odds are low. But if you’re a business owner filing a Schedule C, earning over $400,000, or have a history of mismatched income documents, those odds jump fast. And the IRS plans to push audit rates even higher for high earners through 2026.

This article covers what a tax audit actually is, who the IRS targets, the types of audits you could face, and what it costs if you get it wrong. We won’t cover state-level audits or international tax issues here. Those are separate animals.

What Is a Tax Audit?

A tax audit (the IRS officially calls it an “examination”) is a review of your financial records to verify that what you reported on your return matches reality. The IRS checks your income, deductions, credits, and anything else that affects your tax bill. It applies to individuals, self-employed filers, partnerships, S-corps, C-corps, and any other entity that files a return.

A tax audit isn’t always a sign you did something wrong. Sometimes your return gets flagged by an algorithm. The IRS uses the Discriminant Function System (DIF), which scores returns based on how likely they are to contain errors. If your score crosses a threshold, your return goes to a human reviewer. Other times, a mismatch between your W-2 or 1099 forms and what you reported triggers the review automatically. Elizabeth Young, Director of Tax Practice & Ethics at AICPA, confirmed in a February 2025 CNBC interview that underreported income via information returns remains the top flag. The AICPA itself submitted 183 recommendations for the IRS 2025–2026 guidance plan, focused partly on reducing unnecessary examinations through better IRS clarity.

I’ve seen people panic when they get the letter. Most of the time, the IRS wants documentation for a specific line item. Not a full investigation of your entire financial life.

Why the IRS Audits Tax Returns

The IRS audits returns for three reasons, and only one of them gets talked about.

The obvious reason: making sure people pay what they owe. The IRS closed 505,514 audits in FY 2024 and recommended over $29 billion in additional tax (IRS Data Book 2024). The second reason is deterrence. If nobody ever gets audited, compliance drops. The IRS knows this. Even a low audit rate keeps honest reporting as the default. Understanding the purpose of an IRS audit matters more than most people think.

The third reason is one most articles skip: data collection. Every audit teaches the IRS something about where errors cluster, which industries underreport, and where their algorithms need updating. Your audit isn’t just about you. It feeds the system that decides who gets examined next.

Who Gets Audited by the IRS in 2026?

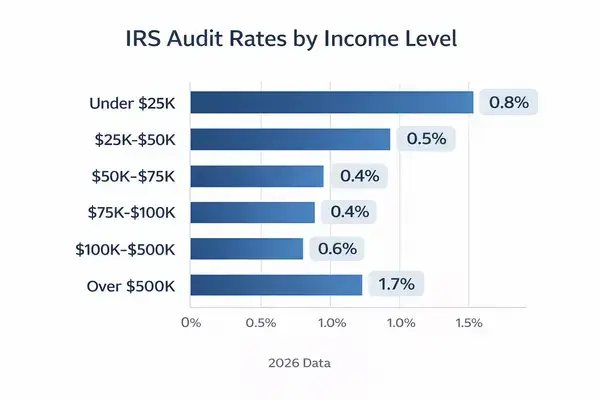

Your audit risk depends on a handful of factors. Income level is the biggest.

If you earn under $400,000 as an individual, the IRS has said repeatedly that it won’t increase audit rates for your bracket. That’s been the policy since 2022, backed by Inflation Reduction Act funding guidelines. But “won’t increase” doesn’t mean “won’t audit.” The baseline rate still applies. Knowing what triggers an audit can help you avoid unnecessary flags.

Where it gets serious is above that line. Returns showing income between $1 million and $5 million had a 1.6% exam rate in recent years. For $5 million to $10 million, that jumped to 3.1%. The IRS plans to push the rate for returns over $10 million to 16.5% by tax year 2026 (up from 11% in 2019). Large corporations with over $250 million in assets face a planned 22.6% rate.

Business owners and self-employed filers sit in a higher-risk category regardless of income. Schedule C returns see audit rates between 0.9% and 1.3%, compared to the overall 0.20%. Cash-heavy businesses and those claiming large deductions relative to revenue draw the most attention.

Specific Triggers That Increase Your Risk

• Income on W-2s and 1099s that doesn’t match your return

• Claiming the Earned Income Tax Credit (historically higher scrutiny)

• Large charitable donations relative to income

• Home office deductions on a Schedule C

• Reporting business losses year after year

• Employee Retention Credit claims (now subject to a 6-year audit window)

One thing most people get wrong: being “honest” on your return doesn’t protect you from an audit. The DIF system doesn’t measure honesty. It measures statistical patterns. If your deductions look unusual compared to others in your income bracket, you’ll get flagged whether you did everything right or not.

The Three Types of IRS Tax Audits

Not all tax audits are equal. The IRS runs three types, and they vary wildly in scope and cost. For a deeper breakdown, Austin & Larson has a full guide on the different types of IRS audits.

Correspondence audits happen by mail. The IRS sends a letter asking for documentation on a specific item. You respond with paperwork, and if the IRS is satisfied, it’s done. These make up the vast majority of exams for lower and middle-income filers. Hiring a professional runs $300 to $1,500.

Office audits require you (or your representative) to visit an IRS office. The examiner will ask questions, review documents, and may dig into multiple areas of your return. Professional help typically runs $1,500 to $4,000.

Field audits are the most intense. An IRS agent comes to your home, business, or accountant’s office, reviews records on-site, and may look at everything. For tips specific to this type, see Austin & Larson’s advice on preparing for an IRS field audit. Professional representation starts at $5,000. Complex business returns run $250 to $600 per hour for a tax attorney.

| Audit Type | How It Works | Cost for Professional Help | Timeline |

| Correspondence | Mail-based, specific items | $300 – $1,500 | Weeks to months |

| Office | In-person at IRS office | $1,500 – $4,000 | 1–3 meetings + prep |

| Field | Agent visits your location | $5,000+ | Several months |

I’ve worked with clients who tried to handle a field audit alone and ended up agreeing to assessments they could have fought. Self-representation has a place in correspondence audits. Anything beyond that, you’re outmatched.

Choosing the Right Representative

Three types of professionals can represent you before the IRS: enrolled agents (EAs), certified public accountants (CPAs), and tax attorneys. If you’re unsure whether you need a lawyer for your audit, the answer depends on the complexity of your case.

Enrolled agents have unlimited IRS representation rights and usually charge $1,700 to $5,500 for individual and business audits. CPAs offer similar representation at comparable rates. Tax attorneys step in for complex disputes, appeals, or cases heading toward litigation, billing $5,000 to $15,000 or more.

Here’s the contrarian take: most people don’t need a tax attorney for a standard audit. An experienced enrolled agent will get the same result for a fraction of the cost. The exception is if you’re facing potential fraud allegations, criminal referral, or a dispute large enough for Tax Court. Then you absolutely need a lawyer. Working with a team that understands IRS procedures from the marketing side can also help firms like Austin & Larson reach the people who need this kind of help.

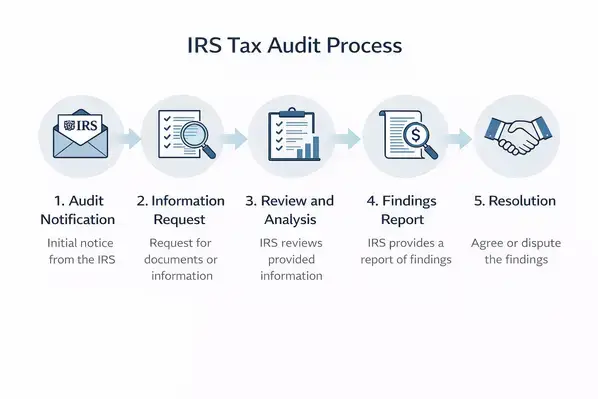

How the Tax Audit Process Works

The process follows a predictable path.

First, you receive a notice by mail. The IRS never starts an audit by phone or email. If someone calls claiming to be from the IRS and says you’re being audited, that’s a scam. The notice tells you which type of audit it is, which tax year is under review, and what documents you need.

For correspondence audits, you gather the requested records, attach them to your response, and mail everything back within the deadline (usually 30 days). Office and field audits require more preparation: bank statements, receipts, contracts, and anything that supports the numbers on your return.

If you disagree with the auditor’s findings, you have the right to appeal. The IRS Independent Office of Appeals handles these cases, and you don’t need to go to court to dispute a result. In many situations, the appeals process produces a better outcome than the initial exam. If you designate a representative, they’ll need a signed Form 2848 (Power of Attorney) before they can talk to the IRS on your behalf. Get this done before the audit starts, not after. For a step-by-step walkthrough, see Austin & Larson’s guide on steps to take after receiving an audit.

Tax Audit Deadlines and Statutes of Limitations

The IRS generally has three years from the date you filed your return to start an audit. This is the statute of limitations for assessment.

But there are exceptions that stretch that window. If you underreported income by more than 25%, the IRS has six years. If you filed a fraudulent return or didn’t file at all, there’s no time limit. Employee Retention Credit claims now carry a six-year audit window as well.

When you receive an audit notice, you typically have 30 days to respond. Missing that deadline can result in the IRS issuing a default assessment based solely on their calculations, which almost always costs more than it should. If you need more time, you can request an extension. Austin & Larson has more detail on valid reasons to extend a tax audit.

What Happens If You Ignore a Tax Audit Notice?

This is where people hurt themselves the most.

In FY 2024, the failure-to-respond rate for low-income audit cases hit 53.7%, per the Taxpayer Advocate 2024 Annual Report. Over half the people audited in that bracket simply didn’t reply. The result? Full assessments, penalties, and zero chance to argue the numbers.

What might have been a $2,000 adjustment can balloon to $5,000, $10,000, or more once the IRS adds accuracy penalties (20% of the underpayment) and failure-to-respond consequences on top. For a full breakdown, see Austin & Larson’s guide to the most common IRS penalties.

If you can’t meet the deadline, call the IRS and ask for an extension. They’ll usually grant it. Silence is the worst move you can make.

Lowering Your Audit Risk

You can’t guarantee you’ll never be audited. But you can reduce your odds.

Keep records that match every line on your return. If you claim a deduction, have documentation for it. Receipts, bank statements, contracts. The IRS denies deductions it can’t verify. Austin & Larson has a detailed guide on keeping accurate records for tax purposes that’s worth reading.

File electronically and on time. Paper returns have a higher error rate, and late filings draw additional scrutiny.

If you’re self-employed, report all income, even amounts under the 1099 reporting threshold. The IRS receives copies of payment records from platforms and clients. Mismatches are the single easiest trigger for an automated review.

And here’s the advice I give every business owner: don’t claim deductions you can’t defend under questioning. I’ve seen people claim a home office that’s actually a guest bedroom, or write off a “business lunch” that was dinner with their spouse. Those deductions aren’t worth the risk. The money you save on your return is nothing compared to what you’ll spend defending a tax audit.

FAQs

How likely am I to get audited by the IRS?

The overall individual audit rate was roughly 0.20% in FY 2024, or about 2 out of every 1,000 returns filed. Your risk increases with income. Returns over $10 million face a planned 16.5% audit rate by 2026. Business owners filing Schedule C see rates between 0.9% and 1.3%.

Can I represent myself in a tax audit?

You can, but it’s risky beyond a simple correspondence audit. In FY 2024, the failure-to-respond rate for low-income audits was 53.7%. Professional representation typically costs $300 to $15,000 depending on the audit type and reduces the chance of overpaying by 30% to 70%.

What’s the difference between a correspondence audit and a field audit?

A correspondence audit happens by mail and focuses on one or two specific items. A field audit involves an IRS agent visiting your home or business to review everything. Correspondence audits cost $300 to $1,500 to resolve with professional help. Field audits start at $5,000.

How far back can the IRS audit my tax returns?

The standard window is three years from the date you filed. If you underreported income by more than 25%, the IRS gets six years. For fraudulent returns or unfiled returns, there is no time limit. ERC claims now face a six-year window as well.

Does audit protection from tax software actually work?

Most “audit protection” add-ons from tax software cover basic correspondence support but not full representation for complex disputes. Professional resolution for an office or field audit still costs $1,500 to $15,000. The add-on is marketing, not legal protection.

Should I hire an enrolled agent or a tax attorney for my audit?

An enrolled agent handles most individual and business audits effectively at $1,700 to $5,500. A tax attorney is the better choice for fraud allegations, Tax Court cases, or disputes involving $50,000 or more. For a standard correspondence or office audit, an enrolled agent is usually the smarter financial move.

What happens if I ignore an IRS audit letter?

The IRS will issue a default assessment based entirely on their calculations, which is almost always higher than what you’d owe with proper documentation. Penalties for underpayment (20% accuracy penalty) and failure to respond stack on top. A $2,000 issue can easily become $10,000 or more.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments