Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: June 30, 2026

Most tax-relief ads skip this number. The IRS accepted about 21% of offers in compromise in 2024, down from 42% a year earlier, with early 2025 near 14%. If you are counting on an offer in compromise to erase your tax debt, the odds are not good and falling.

Below: your real odds, who qualifies, why the IRS says no, and what to do instead, minus the “pennies on the dollar” fantasy.

What Is an Offer in Compromise?

An offer in compromise is a deal with the IRS that lets you settle a tax debt for less than you owe. You propose a figure, the IRS weighs your income, assets, and expenses, then accepts, rejects, or counters.

In 2024 the IRS issued more than 50.7 million civil penalties. An offer is one way out, but not the only one, and for most people not the first to try.

How Often Does the IRS Accept an Offer in Compromise?

Not often, and falling. About 21% of offers were accepted in 2024, down from 42% in 2023, with early 2025 near 14%.

The counts: in 2023 the IRS received 30,163 offers and accepted 12,711; in 2024, 33,591 received and 7,199 accepted.

Zoom out: from 2015 through 2024, taxpayers filed 499,095 offers and the IRS approved 183,407, a 36.7% rate, about one in three. The recent trend is closer to one in five. Erin Collins, the National Taxpayer Advocate, warned in her January 2026 report to Congress that a 27% workforce cut and sweeping tax-law changes make 2026 tougher on taxpayers.

Do You Actually Qualify for an Offer in Compromise?

Clear a basic gate first. Miss one item and your file is bounced without review. You qualify to file only if all of this holds:

- You have filed every required return and made your estimated payments.

- The IRS has billed you for at least one covered debt.

- You have paid the $205 fee, or qualify for a waiver.

- You included your first payment with the application.

- You have a valid extension if the current year is included.

- With employees, you are current on federal deposits for two quarters.

- You are not in an open bankruptcy.

Even then, the IRS approves on one of three grounds: doubt you owe it, doubt it can collect it all, or proof that full payment would be unfair. For almost everyone it is the second, and it comes down to one number.

How Does the IRS Decide What Your Offer Should Be?

The IRS runs a formula called Reasonable Collection Potential, or RCP. Your offer must meet or beat it, or it is dead on arrival.

RCP adds two things: the quick-sale value of what you own, about 80% of market value after loans (home equity, vehicles, accounts, retirement), plus your future income minus IRS-allowed living expenses over a set number of months.

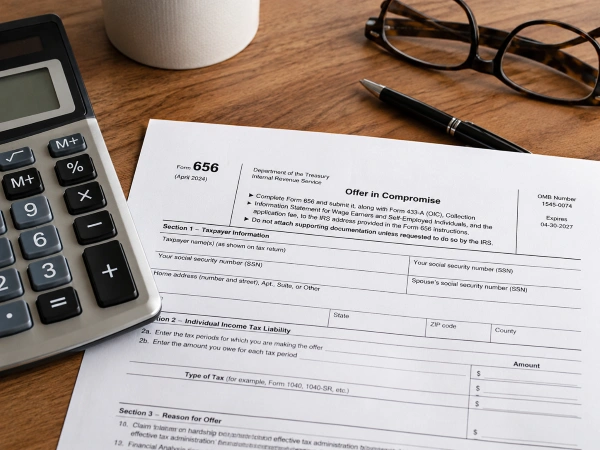

One detail trips people up: those allowed expenses follow IRS standards that shift by location. In a higher-cost Michigan county, housing and transportation allowances run higher than in a rural area, which lowers your RCP. A stronger application starts with this math, run before you file. You submit it on Form 656-B. Test your numbers in the IRS pre-qualifier tool first.

The IRS is not giving you a discount; it accepts the most it thinks it can collect anyway, so anything below that gets rejected.

Why Does the IRS Reject an Offer in Compromise?

Most rejections trace to three things: you did not qualify, your paperwork was incomplete, or your offer fell below what the IRS could collect.

Fall behind on this year’s return or payments and you are out before review. Sloppy financials kill the rest: missing bank statements, unexplained expenses, asset values that do not match reality. I have watched offers die over one missing statement. And if a monthly payment plan could clear the debt, the IRS takes that over a settlement.

The IRS also warns about offer mills, the outfits advertising debt settled for pennies. They take a fee up front, file a generic offer that often had no shot, and keep the money whether you win or not. A firm advertising 90% acceptance screens out weak cases first, so its number looks nothing like the real 14% to 21%. Judge the lawyer, not the ranking.

Can You Appeal a Rejected Offer in Compromise?

Yes. You have 30 days from the date on your rejection notice to appeal, worth doing when the IRS misread your finances.

Your appeal states who you are, what you dispute, why, and any supporting tax law. The strongest show a mis-valued asset, overstated income, or special hardship.

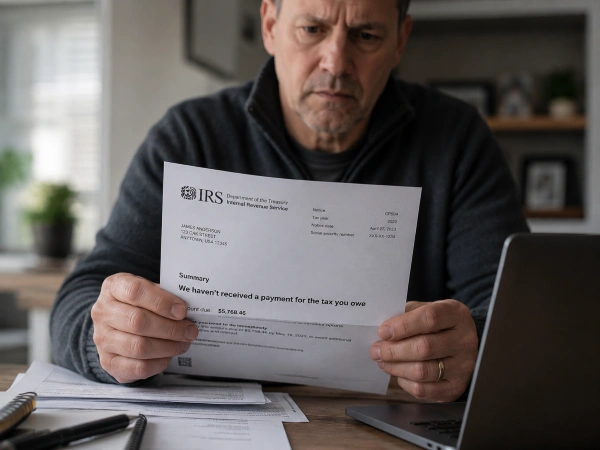

In 2024 the IRS received 3,805 OIC appeals and closed 5,276, working down older cases. Miss the window and collection resumes: wage garnishment, bank levies, or a federal tax lien on your property. Do not sit on a rejection notice.

Better Options Than an Offer in Compromise for Most People

For most people, one of these beats an offer. The IRS often rejects an offer in compromise exactly because a simpler tool fits.

| Option | What it does | Best for | What it costs you |

|---|---|---|---|

| Offer in compromise | Settles debt for less than owed | Provable inability to pay | $205 + 20% down; low approval |

| Installment agreement | Monthly payments over time | Steady income over years | Setup fee; interest runs |

| Currently Not Collectible | Pauses collection in hardship | No room to pay now | Free; debt and interest remain |

| Penalty abatement | Erases certain penalties | First-time slip or good cause | Free to request |

| Innocent spouse relief | Removes a spouse’s debt | Joint debt that is not yours | Free to request |

| Bankruptcy | Discharges some older tax debt | Debt meeting timing rules | Court and attorney fees |

An installment agreement is the workhorse: with steady income, the IRS almost always grants a monthly payment plan, with far better odds than any offer.

One Michigan trap: a federal offer does nothing for state tax debt. Owe the Michigan Department of Treasury and that is a separate process. People settle with the IRS, then get a state notice months later.

FAQs

What is the success rate of an offer in compromise right now?

Around 21% in 2024, down from 42% in 2023, with early 2025 near 14%. The ten-year average is about 36.7%. Your odds hinge on whether your offer matches the IRS collection math.

How long does an offer in compromise take?

Up to 24 months. If the IRS does not rule within that window the offer is automatically accepted, but backlogs push most cases to the back end, so do not bank on it.

Can I get my fee and down payment back if I am rejected?

No. The 205 dollar fee and initial payment are nonrefundable, and the IRS applies your payment to the balance even after a denial. Filers at or below 250% of the federal poverty line can have both waived.

Should I hire a lawyer for an offer in compromise?

It depends on the size of the debt. For a small balance, a pro may cost more than you save. For larger or complex cases, a tax attorney or enrolled agent can sharpen your paperwork and odds.

What happens after the IRS accepts my offer?

You are on a five-year leash: file and pay on time for five years, or the IRS can void the deal and restore the full balance plus interest. Acceptance starts the compliance clock, it does not end it.

Run the math before you spend a dollar. An offer in compromise fits a narrow group who truly cannot pay and can prove it; for everyone else, an installment agreement or Currently Not Collectible status does more good with better odds. If the debt is large, find a Michigan tax attorney who will tell you the truth instead of selling a settlement. A 14% acceptance rate is not a reason to quit, just a reason to file only when yours pencils out.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments