Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 14, 2026

Bankruptcy can wipe out some IRS tax debt, but only income taxes that meet four strict timing rules, and only if you’ve been honest with the IRS. Everything else (payroll taxes, fraud penalties, anything assessed in the last 240 days) survives the discharge.

In 2025, U.S. courts logged 574,314 bankruptcy filings nationally, up 11% from 2024. A growing share carry IRS debt. Most don’t need to file. They need to know what kind of tax debt they have.

This guide covers what discharges, what doesn’t, and the 3-2-240 rule. State discharge and non-tax bankruptcy are separate topics.

How Bankruptcy Works When IRS Debt Is in the Picture

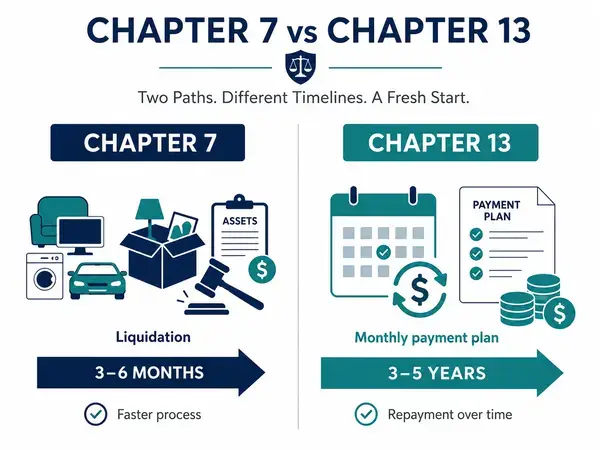

Bankruptcy is a legal reset, not a punishment. Two chapters cover most IRS debt cases: Chapter 7 (liquidation, 3-6 months) and Chapter 13 (repayment plan, 3-5 years).

Chapter 7 wipes out qualifying debts if you pass the means test. Chapter 13 spreads non-dischargeable debt across a court-supervised budget. Sole props and partnerships use the same two chapters; bigger entities use Chapter 11.

One piece worth knowing. The moment you file, the automatic stay kicks in. IRS levies stop. Wage garnishments stop. Lien filings stop. Even when your debt won’t discharge, you buy breathing room.

What Types of IRS Tax Debt Can Be Discharged?

Only federal income tax qualifies, and only when it’s old enough and clean enough. Payroll taxes, trust fund recovery penalties, fraud penalties, and recent assessments don’t discharge at all.

Bankruptcy can discharge older federal income tax debt if the return was due at least three years before filing, was actually filed at least two years before filing, and was assessed by the IRS at least 240 days before filing. Trust fund payroll taxes, civil fraud penalties, and tax debt tied to willful evasion are never dischargeable. Everything else is footnotes.

I’ve reviewed dozens of transcripts where filers assumed all their IRS debt would clear. About half the time, the bulk was payroll-related. They filed anyway and walked out still owing most of it.

Can Bankruptcy Actually Clear Your IRS Tax Debt?

Sometimes. Not often, and not for the reasons most people expect. Roughly 20-40% of IRS Offer in Compromise applications get accepted in a given year, and bankruptcy is even more selective for tax discharge.

The reason isn’t IRS strictness. It’s filing behavior. The biggest dealbreakers are unfiled returns, recent assessments, and trust fund taxes.

Contrarian take. Tax relief firms market bankruptcy as a last resort. For filers with older income tax debt, returns filed on time, and no audit drama, bankruptcy is actually the first option to consider. It’s a permanent, court-ordered discharge rather than a negotiated settlement that can fall apart if you miss a payment.

Inside the 3-2-240 Rule for Tax Discharge

The 3-2-240 rule is what bankruptcy courts use to test whether income tax debt qualifies for discharge. Every year of tax debt gets tested separately. Some years can clear while others stay. The four requirements:

• Three-year rule. The return must have been due (including extensions) at least three years before your filing date.

• Two-year rule. You must have actually filed the return at least two years before bankruptcy. Substitute returns the IRS files for you don’t count.

• 240-day rule. The IRS must have assessed the tax at least 240 days before your filing. Audits and offers in compromise can suspend this clock.

• No fraud or willful evasion. If the IRS proves fraud or willful tax evasion, the debt sticks regardless of age.

Worth correcting a common misread. People hear 3-2-240 and think it’s a pass-fail checklist for the whole filing. It’s not. Each tax year is tested individually.

For the official source, IRS Publication 908 (updated December 2025) walks through every edge case worth knowing.

What Happens If Your Tax Debt Doesn’t Qualify?

Bankruptcy still helps, just differently. Chapter 13 lets you spread non-dischargeable tax debt across three to five years of court-supervised payments, with the IRS frozen out of collection during the plan.

That’s where the automatic stay earns its keep. No bank levies. No wage garnishments. No new federal tax liens during the plan. Once Chapter 13 ends, income tax that qualified under 3-2-240 gets wiped. The rest still has to be paid.

For most people in this bucket, an IRS installment agreement or Fresh Start program is faster and cheaper. The Bankruptcy Court Miscellaneous Fee Schedule lists Chapter 7 at $338 and Chapter 13 at $313, before attorney fees. If your debt is under $50,000 and you can pay it down in 72 months, skip bankruptcy.

How Bankruptcy Hits Business Owners Differently

Business owners face a brutal carve-out. Trust fund recovery penalties are never dischargeable. Ever. In any chapter.

The trust fund recovery penalty is personal liability the IRS assesses on owners and officers who failed to remit payroll withholding. The IRS treats withheld payroll tax as money held in trust for employees and the government. If it doesn’t get remitted, the IRS can pierce the corporate veil and come after the owner personally.

I’ve worked with small business owners who didn’t know this until after they filed Chapter 7. They cleared personal credit card debt and walked out with $80,000-plus in payroll tax liability still attached. Some could have qualified for an Offer in Compromise. Payroll tax problems need a different playbook.

Why Filing Tax Returns Still Matters After Bankruptcy

Filing bankruptcy doesn’t pause your filing obligation. The court will require all returns for the last four years to be filed before it confirms any plan.

Skipping returns is the fastest way to disqualify yourself from discharge. The two-year rule already says substitute returns the IRS prepares for you don’t count. If you have unfiled returns from 2022 sitting around and you file bankruptcy in 2026, those years aren’t going to discharge no matter how old they get.

A separate bankruptcy estate may be created for tax purposes, with its own Form 1041 obligation. Working with a firm that handles both bankruptcy and tax cuts the risk of a procedural mistake costing you discharge eligibility. For tax practitioners reading this, the other half is partnering with a marketing partner that understands the legal and financial space so the right clients can find you.

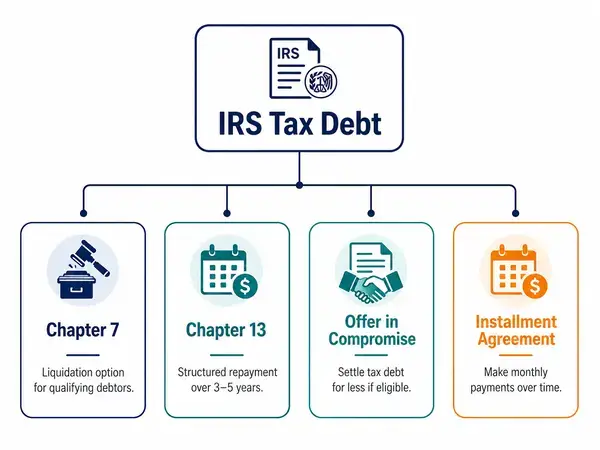

Bankruptcy vs. Other IRS Debt Solutions in 2026

Bankruptcy is one of four serious options for IRS debt resolution in 2026. The right pick depends on debt type, age, and your monthly cash flow.

| Option | Best For | Time Frame | Tax Debt Cleared |

| Chapter 7 Bankruptcy | Older qualifying income tax debt | 3-6 months | Yes (if 3-2-240 met) |

| Chapter 13 Bankruptcy | Mixed dischargeable / non-dischargeable | 3-5 years | Partial |

| Offer in Compromise | Inability to pay full balance | 6-24 months | Settled below balance |

| Installment Agreement | Debt under $50K, steady income | Up to 72 months | Full payment, no discount |

Per IRC §108, debt discharged in bankruptcy is excluded from gross income, so there’s no surprise 1099-C tax bill the following year.

The biggest mistake I see: filers picking a bankruptcy filing for IRS tax debt without first checking which years actually qualify. Spending court and attorney fees to discharge $2,000 in credit card debt while leaving $40,000 in payroll taxes intact isn’t relief. Run the 3-2-240 analysis on each tax year before pulling the trigger.

Pick the right tool and bankruptcy and IRS tax debt becomes a story about a clean slate. Pick the wrong one and it becomes the second-most-expensive mistake of your financial life.

FAQs

Does bankruptcy create a new tax bill on canceled debt?

No. Debt discharged in bankruptcy is explicitly excluded from gross income under IRC §108(a)(1)(A). There’s no surprise Form 1099-C tax bill in the following year for the discharged amount. IRS Publication 908 (December 2025) confirms this directly.

Can I file bankruptcy with unfiled tax returns?

You can file, but those tax years won’t discharge. The two-year rule requires the return to have been actually filed at least two years before your bankruptcy date, and substitute returns the IRS files for you don’t count. Courts will also require the last four years of returns to be filed before confirming any plan.

What happens to my IRS tax debt if it’s payroll-related?

Payroll taxes are never dischargeable in bankruptcy. This includes trust fund recovery penalties personally assessed against business owners and officers who failed to remit withholding. Bankruptcy halts collection during the case via the automatic stay, but the debt itself survives the discharge.

How old does my tax debt have to be to discharge in bankruptcy?

The 3-2-240 rule applies. The return must have been due (with extensions) at least three years before filing, actually filed at least two years before filing, and assessed by the IRS at least 240 days before filing. Each tax year is tested separately, so older years can discharge while newer years stay.

Does the Fresh Start program work after filing bankruptcy?

An active bankruptcy case disqualifies most Fresh Start options, including streamlined installment agreements and Offer in Compromise. After discharge, remaining non-dischargeable tax debt may be eligible for Fresh Start. The IRS Tax Debt Help tool launched in April 2026 walks through current options.

What happens to IRS liens during bankruptcy?

The automatic stay halts new lien enforcement and prevents new lien filings during the case. Existing liens attached to property generally survive bankruptcy even if the underlying personal liability discharges. The IRS Insolvency Department releases liens after discharge for properly cleared tax debt, usually within 30-60 days.

Can a business owner discharge trust fund taxes personally?

No. Personal liability for withheld payroll taxes survives bankruptcy indefinitely in every chapter. Owners and officers who failed to remit employee withholding to the IRS retain that personal liability after discharge. Alternative resolution paths (Offer in Compromise, installment agreement) usually fit this scenario better than bankruptcy.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments