Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 12, 2026

For most W-2 earners taking the standard deduction, tax planning isn’t worth the fee. For business owners pulling $200K+ in revenue, real estate investors, and anyone with $150K+ AGI and serious investments, the math flips hard. Tax planning fees run $1,500 to $15,000 per engagement depending on scope, and for the right situations the savings beat the fee year after year. That’s not marketing math. That’s what shows up on the next tax return.

So which side of that line are you on? Let’s break it down.

What tax planning actually is. Tax planning means a year-round strategy that lowers your future tax bill through specific moves: entity selection, retirement contributions, timing of income and deductions, depreciation choices, charitable bunching, and Roth conversions. It’s different from tax prep, which just files what already happened. Planning shapes the numbers before they hit the return. Most people pay for prep and call it planning, and unless you’re working with experienced Michigan tax professionals, that distinction never gets drawn for you. That’s the first mistake.

How Much Does Tax Planning Actually Cost in 2026?

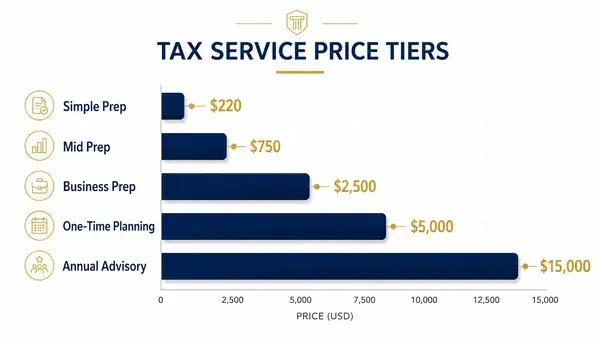

Real ranges, based on national data from 2025 to 2026:

| Service Type | Cost Range | Who It Fits |

| Simple W-2 prep only | $220–$400 | Standard deduction filers |

| Mid-complexity prep (itemized, investments) | $400–$800 | Homeowners, mid-income |

| Business or multi-state prep | $800–$1,500+ | Schedule C, rentals, K-1s |

| One-time tax planning engagement | $1,500–$5,000 | Mid-complexity individuals |

| Annual advisory + planning | $5,000–$15,000 | Business owners $200K+ revenue |

Sources: IBISWorld Accounting Services 2026 industry data and the NATP 2025 Fee Study.

Per the same NATP 2025 Fee Study, the CPA flat fee for a Form 1040 with Schedule A and a state return averaged $323. Hourly CPA rates run $200 to $500 depending on credential and region. The Northeast and California come in 30 to 50% above Midwest pricing for similar work. None of that matters if your return fits on one page and you’re using software.

When Is Tax Planning Worth It for You?

The honest answer: when the planner can find more than their fee in savings, year after year, with reasonable confidence. That’s almost never true for simple returns and almost always true above certain thresholds.

I’ve watched this pattern repeat across enough clients to call it. The break-even point sits roughly where complexity stacks up: multiple income types, deductible business expenses, retirement accounts, real estate, or a partnership return. Hit two of those and a mid-range planning fee usually pays for itself in year one.

Do You Own a Business?

If your business pulls more than $200K in revenue, yes. Without question.

Pass-through entities (LLCs taxed as partnerships, S-corps, sole props) push income onto your personal return, which means your business decisions are tax decisions whether you treat them that way or not. The biggest leak I see in mid-sized businesses: skipping S-corp reasonable compensation analysis and missing the 20% QBI deduction under Section 199A. Both are verifiable wins under current code, but the elections, timing, and entity choices that decide how much you actually pay aren’t on the return. They happen before it. There’s a reason Michigan business tax help often produces the highest planning ROI of any category.

Software won’t catch the missed elections. The IRS won’t volunteer the corrections.

Investment Properties Change the Math

Yes, if you own more than one rental or carry depreciation across multiple years.

Cost segregation alone reclassifies portions of a building’s basis into shorter-life assets, accelerating depreciation into the early years instead of stretching it across 27.5 or 39 years. Add a 1031 exchange to defer gains on a sale and the planning fee disappears in the rounding.

Rental property owners who file Schedule E without a planner usually miss passive activity grouping elections, real-estate-professional status, and the QBI safe harbor for rentals. Each of those is its own missed five-figure deduction.

Are You Planning for Retirement?

If you’re within ten years of retirement and have more than $250K across retirement accounts, tax planning matters more than your asset allocation.

The big levers for 2026, per IRS Notice 2025-67 and Revenue Procedure 2025-19: 401(k) elective deferrals at $24,500 (catch-up $8,000 if 50+, plus an $11,250 super catch-up for ages 60 to 63 under SECURE 2.0), traditional and Roth IRA limits at $7,500 ($8,600 with catch-up), and HSA limits at $4,400 single / $8,750 family. Roth conversions during low-income years between retirement and required minimum distributions can save tens of thousands across a 20-year horizon, depending on the bracket gap. Qualified Charitable Distributions from IRAs after age 70½ count toward your RMD without hitting AGI. Inherited IRA tax rules also play here, especially under the 10-year payout rule. None of this gets surfaced by filing software, which is why retirees with complex distributions often work with a Michigan tax attorney team that can model the full picture.

How the New OBBBA Tax Law Affects You

Yes, and most filers haven’t caught up.

The One Big Beautiful Bill Act, signed July 4, 2025, made the lower TCJA individual brackets permanent (top rate stays at 37%), kept the larger standard deduction, and locked in the Section 199A pass-through deduction. It also brought back 100% first-year deduction for most qualified property placed in service after January 19, 2025. The strategic shift: with brackets now permanent, the urgency around Roth conversions drops some, but inflation-adjusted bracket creep and the new business expensing rules open fresh planning windows. The AICPA released its Top 40 Tax Planning Opportunities for 2026 in March 2026 specifically to address post-OBBBA strategy, and the Tax Foundation’s nonpartisan breakdown covers the long-term impact for individual filers.

When Is Tax Planning NOT Worth the Fee?

This is the part most articles skip. If you’re a W-2 earner with no side income, no rental property, no investments outside a 401(k), and you take the standard deduction, paying $2,000 for a planning engagement is a waste. Software handles your situation fine. The planner will hand you a Roth IRA recommendation, a 401(k) max-contribution suggestion, and maybe an HSA pitch, then bill you $2,000 for advice you could get from any decent finance podcast.

The trap: planners who sell engagements to people who don’t need them. Watch for flat-fee “tax planning packages” pushed at every income level. If your effective tax rate is already under 12% and your return fits on a single page, walk away.

About 45% of Americans file completely DIY, according to IRS FY 2024 data. For most of them, that’s the right call. Roughly 55% get some form of professional help, and within that group, only a fraction need full advisory work. The rest just need clean prep and solid tax compliance habits.

How Do You Choose the Right Tax Planner?

Three credentials matter:

• CPA: Broadest scope. Handles audits, attest work, and full planning. Best fit for business owners.

• EA (Enrolled Agent): Federally licensed, focused purely on tax. Often cheaper than a CPA for the same planning work.

• Tax attorney: Needed only when there’s a legal dispute, an estate tax issue, or complex entity restructuring.

Ask three questions before signing an engagement letter. What’s your multi-year projected effective rate under their plan versus your current one. Will the engagement include strategy memos and projections, or just filing. What’s their fee for the first year versus ongoing. If they can’t answer with specifics, keep looking. Working with a marketing partner who knows the financial services vertical follows the same principle on the agency side: generic shops can’t compete with operators who know the niche.

Practitioner forums share a consistent tell for spotting real planning: multi-year scenario modeling. If your CPA only shows you this year’s number, they’re filing, not planning.

Getting Started

If you own a business, hold investment property, or sit within ten years of retirement with serious account balances, the math on tax planning works in your favor almost every year. If your return is simple, skip the fee. Walk in with the questions above, ask for the projected effective rate, and don’t pay for a planning package that’s really just prep with a higher price tag.

For Michigan filers dealing with complex situations or IRS issues, the Austin & Larson team handles planning work and the cleanup when planning didn’t happen in time. Reach out for a consultation and we’ll show you the math before you commit to anything.

FAQs

How much does professional tax planning cost in 2026?

Tax planning fees in 2026 run $1,500 to $5,000 for a one-time engagement and $5,000 to $15,000 for ongoing annual advisory. Basic tax prep is separate and ranges from $220 to $1,500 depending on complexity. According to the NATP 2025 Fee Study, the CPA flat-fee average for a Form 1040 with Schedule A and a state return is $323.

Is tax planning worth it if I’m not a business owner?

For most W-2 employees taking the standard deduction, no. But if your AGI is above $150,000, you hold significant investments, or you’re within ten years of retirement with $250K+ in retirement accounts, planning fees typically pay for themselves through bracket management, Roth conversions, and timing strategies.

What changed with the OBBBA tax law for 2026 planning?

The One Big Beautiful Bill Act, signed July 4, 2025, made the lower TCJA brackets permanent (top rate 37%), kept the larger standard deduction, locked in the Section 199A pass-through deduction, and brought back 100% first-year deduction for qualified property placed in service after January 19, 2025.

How do I know if my CPA is doing real tax planning or just filing returns?

Real planning includes multi-year projections, written strategy memos, and modeling of effective tax rates under different scenarios. If your CPA only delivers a completed return and doesn’t show you 3 to 5 year projections, you’re paying for filing, not planning. Ask specifically for QBI and Section 199A modeling.

What’s the typical ROI on tax planning fees?

ROI on tax planning varies sharply by situation. For W-2 employees with simple returns, ROI is often negative because the planner’s value adds little beyond what software delivers. For S-corp owners with $200K+ in revenue, retirees coordinating Roth conversions, and real estate investors using cost segregation or 1031 exchanges, multi-year ROI in the high single-digit multiples is realistic. Ask any planner for projected savings in writing before signing an engagement letter.

Should I bunch deductions or defer income in 2026?

With OBBBA making brackets permanent, the strategy depends on your situation. Bunching itemized deductions into a single year remains useful for taxpayers near the standard deduction threshold. Income deferral makes sense if you expect to drop a bracket in 2027 due to retirement, business sale, or lower revenue.

CPA vs EA vs tax attorney: who handles tax planning?

CPAs offer the broadest scope and are the standard fit for business-owner planning. Enrolled Agents (EAs) are federally licensed tax specialists and often charge less than CPAs for similar planning work. Tax attorneys are only needed for legal disputes, estate tax issues, or complex entity restructuring.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments