Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: April 14, 2026

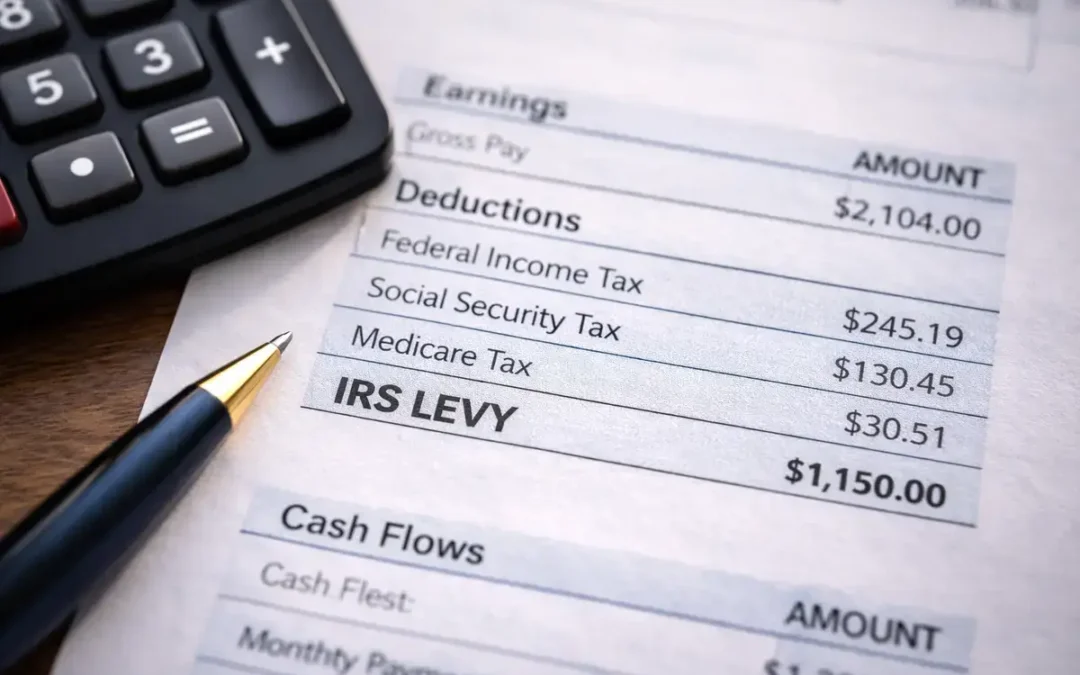

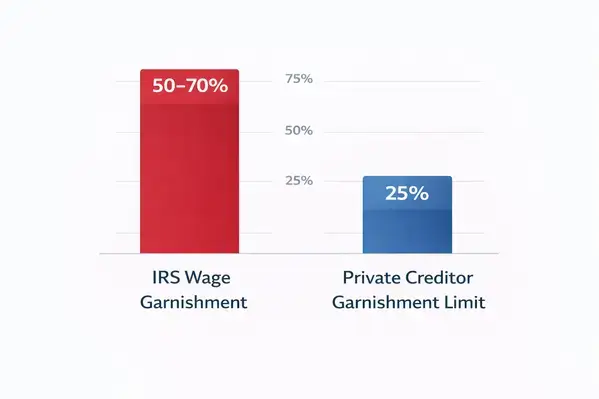

The IRS doesn’t follow the same rules as credit card companies or debt collectors. While most creditors are capped at 25% of your disposable earnings, the IRS can take everything above a fixed exempt amount. For a single filer with no dependents earning $1,000 per week in 2026, the IRS keeps roughly $690, leaving you just $309.62. That’s about 69% of your paycheck, gone before you see it. The actual amount depends on your filing status, the number of dependents you claim, and how often you’re paid. Those numbers come from IRS Publication 1494, updated every December for the following tax year.

IRS wage garnishment (also called a wage levy) is a legal process where the IRS takes a portion of your paycheck directly from your employer to satisfy unpaid federal tax debt. The IRS is exempt from the Consumer Credit Protection Act’s 25% cap and instead uses fixed exempt-amount tables, often taking 50% to 75% or more of a taxpayer’s net pay.

If you’ve received a “Final Notice of Intent to Levy,” you have 30 days to respond before the IRS starts taking money from every paycheck. I’ve worked with taxpayers who lost two-thirds of their take-home pay because they missed that deadline. This article won’t cover state-level garnishment rules or private creditor levies. We’re focused strictly on what the IRS can do, what you get to keep, and how to stop it.

What Is IRS Wage Garnishment?

A wage levy is the IRS telling your employer to send them a chunk of your paycheck every pay period until your tax debt is paid or you reach a resolution. Your employer has zero say in the matter. Once they get the notice, they comply or face penalties themselves.

The IRS can’t just start garnishing without warning. They follow a specific sequence. First, they’ll send a bill (usually a CP14 notice). If you ignore that, more letters follow. The final step before garnishment is the “Final Notice of Intent to Levy and Notice of Your Right to a Hearing.” That letter triggers a 30-day window. You can request a Collection Due Process hearing, set up a payment plan, or explore tax relief options during that period.

Most people I’ve seen in trouble weren’t blindsided. They got the letters and put them in a drawer. That’s the single most expensive mistake in tax debt.

How Much Can the IRS Take From Your Paycheck?

Under Title III of the Consumer Credit Protection Act, private creditors can only garnish 25% of your disposable earnings (or the amount exceeding 30 times federal minimum wage, whichever is less). The IRS doesn’t follow that rule. They use Publication 1494 tables that set a fixed dollar amount you’re allowed to keep each pay period based on three factors: filing status, number of dependents, and pay frequency.

Everything above that exempt amount goes straight to the IRS.

A single person with no dependents earning $1,000 weekly in 2026 keeps $309.62. The IRS takes $690.38. That’s 69%. A married couple filing jointly with two dependents earning $2,000 weekly keeps $668.26. The IRS takes approximately $1,331.74 (about 67%). These aren’t hypothetical ranges. They’re exact calculations from the 2026 tables (IRS Publication 1494, Rev. 12-2025).

One detail that gets buried in most articles: if you don’t return the “Statement of Dependents and Filing Status” to your employer within three days of the levy notice, the IRS defaults you to married filing separately with zero dependents. That’s the absolute lowest exempt amount on the table. Tax professionals report this as the number-one avoidable error in wage garnishment cases. It can cost hundreds of dollars per paycheck for months or even years.

2026 Wage Garnishment Exemption Amounts

The IRS updates these figures annually for inflation. Below are the weekly exempt amounts for levies served in 2026, pulled directly from Publication 1494 (Rev. 12-2025):

| Filing Status | 0 Deps | 1 Dep | 2 Deps | 3 Deps |

| Single / MFS | $309.62 | $411.54 | $513.46 | $615.38 |

| Married Filing Jointly | $464.42 | $566.34 | $668.26 | $770.18 |

| Head of Household | $411.54 | $513.46 | $615.38 | $717.30 |

Source: IRS Publication 1494 (Rev. 12-2025). Additional exemption for age 65+ or blind: +$78.85/week (single/HOH).

Something the IRS won’t tell you: these exempt amounts are identical whether you live in rural Mississippi or midtown Manhattan. There’s no cost-of-living adjustment. In high-rent markets, these weekly amounts often fall below actual living expenses. The IRS describes the exempt amount as covering basic living needs, but practitioners working with real clients in expensive cities will tell you that framing falls apart fast.

Child Support and Spousal Support Limits

If your child support or alimony comes directly out of your paycheck through a wage deduction, the IRS must reduce its garnishment by that support amount. Your obligations to dependents get priority over the tax debt.

But there’s a catch most people miss. If you make child support payments through lump sums or independent periodic payments (not payroll deductions), the IRS won’t automatically account for them. You have to tell the IRS directly and provide documentation. Skip this step, and they’ll calculate your garnishment as if those support payments don’t exist.

IRS Garnishment for Non-Tax Federal Debts

Wage levies aren’t just for unpaid income taxes. If you’ve defaulted on federal student loans or other government debts, the IRS can garnish up to 15% of your disposable income under the Debt Collection Improvement Act.

And it stacks. Owe back taxes and have defaulted student loans? You could face multiple levies on the same paycheck. The total garnishment still can’t violate the Consumer Credit Protection Act’s overall limits across all creditors, but the IRS levy calculation operates independently. If you’re dealing with overlapping federal debts, a tax attorney who handles IRS negotiations can often consolidate these issues into a single resolution.

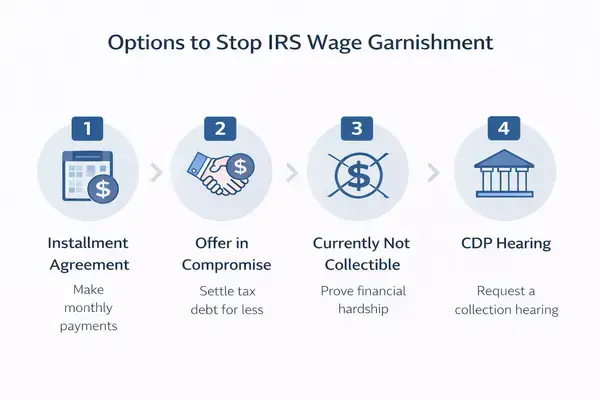

How Do You Stop an IRS Wage Levy?

You’ve got four primary options. The right one depends on your financial situation, and picking the wrong one wastes time you don’t have.

1. Installment agreement. File Form 9465 to set up monthly payments. Once the IRS approves it, they release the levy. You can apply for an installment agreement online if you owe less than $50,000 and can pay within 72 months.

2. Offer in compromise (OIC). This lets you settle tax debt for less than you owe. The IRS accepted roughly 30% of OIC applications in recent years, but the success rate climbs with professional representation. Enrolled agents and CPAs typically charge $2,000 to $10,000+ depending on debt size.

3. Currently Not Collectible (CNC) status. If you can prove that paying would cause genuine financial hardship, the IRS can pause all collection activity. You can request hardship status and get the levy released while your case is reviewed. This is temporary, but it buys breathing room.

4. Collection Due Process (CDP) hearing. If you believe the levy was issued in error or the amount is wrong, request a hearing within 30 days of the final notice. This pauses the levy until the hearing is resolved.

The worst move is doing nothing. Every paycheck that goes by with the levy in place is money you don’t get back. Penalties and interest keep piling on the remaining balance. And in FY 2024, the IRS collected $77.6 billion in previously unpaid taxes (up 13.6% year over year, per the IRS Data Book 2024). They’re collecting more aggressively than ever, and a team experienced in tax resolution strategy can make the difference between months of lost income and a fast resolution.

Bankruptcy as a Last Resort

Filing for Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay that stops IRS wage garnishment immediately. But it doesn’t make the debt vanish. Some income tax debts can be discharged through bankruptcy if they meet specific rules around age, filing history, and assessment dates. Payroll taxes, fraud penalties, and recent tax years typically survive the process.

This option carries long-term credit damage and should be a last resort after you’ve exhausted levy release, installment plans, and OIC paths. Talk to a tax attorney before pulling this trigger.

Take Action Before the IRS Takes Your Paycheck

The maximum amount the IRS can garnish from your paycheck in 2026 isn’t a simple percentage. It’s everything above a fixed exempt amount that shifts based on your filing status, dependents, and pay frequency. For most single filers, that means the IRS can take 50% to 70% of every paycheck until the debt is resolved.

If you’ve received a levy notice, the clock is already running. Acting within that 30-day window is the difference between keeping more of your paycheck and watching the IRS take the maximum the law allows. Don’t be the person who puts the letter in a drawer.

FAQs

Does the 25% garnishment limit apply to the IRS?

No. The 25% cap under the Consumer Credit Protection Act applies to private creditors, not the IRS. The IRS uses fixed exempt-amount tables from Publication 1494 and can take everything above that amount. A single filer with $1,000 in weekly pay and zero dependents keeps only $309.62 in 2026. The IRS takes the rest.

What happens if I don’t return the dependent statement within 3 days?

Your employer defaults your exempt amount to the lowest category: married filing separately with zero dependents. This can cost you hundreds of dollars per paycheck for the entire duration of the levy. Tax professionals consistently report this as the most common avoidable mistake in IRS wage garnishment cases.

Can the IRS garnish my entire paycheck?

Not entirely, but close. The IRS must leave you with the exempt amount based on your filing status and dependents. For some filers, that amount is as low as $309.62 per week (2026 figures). If your net pay is near or below the exempt threshold, the IRS takes very little, but most wage earners lose 50% to 70% of their take-home pay.

Does where I live affect how much the IRS can garnish?

No. The IRS exempt-amount tables are identical nationwide. There is no cost-of-living adjustment. A single filer in San Francisco keeps the same $309.62 per week as a single filer in rural Texas, despite drastically different housing and living costs.

Can the IRS garnish bonuses and commissions?

Yes. Bonuses, commissions, and other forms of compensation are treated as wages under the same Publication 1494 tables. The IRS applies the same exempt-amount calculation to any earnings classified as wages, salaries, or similar compensation.

How long does IRS wage garnishment last?

The levy continues until your tax debt is fully paid, you reach a resolution with the IRS (installment agreement, offer in compromise, or CNC status), or the collection statute expires. The IRS generally has 10 years from the date of assessment to collect, but interest and penalties keep growing the balance during that time.

How do I stop IRS wage garnishment fast?

The fastest path is contacting the IRS (or having a tax professional contact them) to set up an installment agreement or request Currently Not Collectible status. Once approved, the levy is released. Filing for bankruptcy also triggers an immediate automatic stay. Professional representation typically speeds the process from months to days or weeks.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments