The IRS filed 196,996 Notices of Federal Tax Lien in fiscal year 2024, up from 179,019 the year before. That number is climbing as pre-pandemic deferred balances cycle through the collection system. If you’re reading this, you probably have one attached to your name or you’re worried one is coming. Here’s what a federal tax lien actually does, how it differs from a levy, and the specific steps you can take to get it released, withdrawn, or subordinated.

How a Federal Tax Lien Works

A federal tax lien is a legal claim the government places on everything you own when you have an unpaid tax balance. Under Internal Revenue Code §6321, that claim attaches the moment the IRS assesses the tax and you fail to pay after receiving a Notice and Demand for Payment (typically a CP14 notice). It covers real property like your home, personal property like vehicles, and financial assets including bank accounts and investment portfolios.

What makes a lien different from most creditor actions: the IRS doesn’t need to sue you or get a court judgment. The statutory lien arises automatically under IRC §§6321 through 6322. You won’t even know it exists at first. It’s sometimes called a “silent lien” for that reason.

The lien becomes public when the IRS files a Notice of Federal Tax Lien (Form 668(Y)) with your county recorder’s office. This filing is what shows up on background checks and alerts other creditors that the government has priority interest in your property. The IRS typically files in the county where you live and may file in additional counties where you hold assets. If you owe back taxes and aren’t sure whether a lien has been filed against you, Austin & Larson Tax Resolution can pull your IRS transcripts and find out.

The Notice Sequence That Leads to a Lien

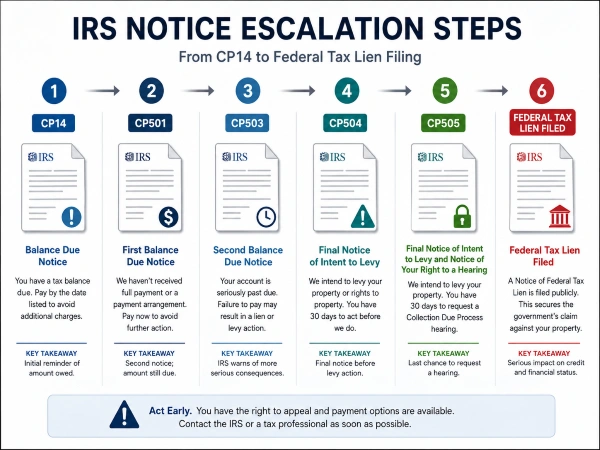

Liens don’t appear out of nowhere. The IRS follows a structured escalation before filing one:

- CP14 is the first bill notifying you of the unpaid balance.

- CP501 is a reminder notice.

- CP503 is a second reminder with more urgent language.

- CP504 is the Notice of Intent to Levy. This is the one that causes most taxpayers to panic.

- Notice of Federal Tax Lien is filed after the IRS considers the debt unresolved.

A critical detail most articles leave out: the IRS often files a lien after establishing a resolution on your account, not just when you’re ignoring them. If you negotiate a currently not collectible status or an installment agreement, the IRS may still file a lien to protect its interest. Being in compliance doesn’t prevent a lien. It prevents a levy.

If you’ve already received a CP14 or CP504, you’re in the escalation window. Getting into a compliant resolution early, particularly a direct debit installment agreement for qualifying balances, can prevent the IRS from filing a Notice of Federal Tax Lien in the first place.

Lien vs. Levy: The Distinction That Matters

A lien secures the government’s interest in your property. A levy actually seizes it.

Think of a lien as a claim staked on your assets. Nobody takes anything from you, but you can’t sell, refinance, or transfer property free and clear until the lien is addressed. A levy, on the other hand, means the IRS is actively taking money from your bank account, garnishing your wages, or seizing physical property. According to the IRS’s own guidance on federal tax liens, a lien secures the government’s interest while a levy actually takes the property to satisfy the debt.

Here’s an example of how this plays out in practice.

Sarah owes $35,000 from unfiled 2019 and 2020 returns. After she files, the IRS assesses the balance and sends a CP14. She hires a tax resolution firm that gets her placed in currently not collectible status because her monthly expenses exceed her income. The IRS agrees she can’t pay right now, but they still file a Notice of Federal Tax Lien in her county.

Six months later, Sarah inherits her mother’s house and decides to sell it. The sale would net her $80,000 after the existing mortgage. Without the lien, she’d pocket all of it. With the lien, there’s no clear title. The $35,000 (plus any accrued penalties and interest) gets paid to the IRS from the sale proceeds before Sarah sees a dime of the remaining balance.

That’s the lien doing exactly what it was designed to do: sitting quietly until there’s something to collect.

How a Lien Damages Your Finances

The financial impact goes well beyond the tax debt itself.

Credit reporting. A filed Notice of Federal Tax Lien becomes public record. While the major credit bureaus stopped including tax liens on consumer credit reports in 2018, lenders conducting thorough background checks or title searches will still find it. For business credit and SBA loans, liens remain directly visible and often disqualifying.

Property transactions. You can’t sell real estate with a lien attached without either paying the debt in full or getting the IRS to agree to a discharge or subordination. This kills deals. Buyers’ title companies will flag it, and closings stall or collapse entirely.

Borrowing power. Mortgage lenders, auto lenders, and banks will typically decline applications when an active federal tax lien exists. Even after it’s resolved, the record of the lien can affect your ability to borrow for years.

Future assets too. Under IRC §6321, the lien attaches to property you own at the time of filing and property you acquire afterward. Buy a car, receive an inheritance, open a new bank account: the lien reaches all of it.

If you owe back taxes and haven’t set up a resolution yet, every month of delay increases the risk of a lien being filed and compounding the financial damage.

One Thing Most People Don’t Know About Lien Amounts

The balance shown on your Notice of Federal Tax Lien doesn’t decrease as you make payments. We see this constantly at our firm: a taxpayer calls saying they still have a $50,000 lien on record even though they’ve paid the balance down to $12,000. The lien amount stays at the original figure until the entire debt across all tax periods covered by that lien is fully satisfied. It’s not a running balance. It’s a snapshot of what you owed when the lien was filed.

This confuses lenders, too. A mortgage underwriter will see the full lien amount on your record and assume you owe the entire sum. That’s why getting a lien released or withdrawn as soon as you qualify matters so much for rebuilding your financial standing.

Five Ways to Deal With a Federal Tax Lien

1. Pay the debt in full. The most direct path. The IRS is required to release the lien within 30 days of full payment. This includes the original tax, penalties, and interest.

2. Direct debit installment agreement. If you owe $25,000 or less in combined tax, penalties, and interest, and you set up a direct debit installment agreement (where payments auto-draft from your bank account), the IRS may withdraw the Notice of Federal Tax Lien. This option came out of the IRS Fresh Start initiative. You’ll need to make three consecutive on-time payments before requesting the withdrawal using Form 12277.

3. Discharge of property. The IRS can remove the lien from a specific piece of property to allow a sale. This doesn’t eliminate the lien entirely. It just clears title on that one asset. You apply using IRS Publication 783 and must demonstrate that the sale is in the government’s interest, usually because the proceeds will partially satisfy the debt.

4. Subordination. This doesn’t remove the lien but allows another creditor, like a mortgage lender, to move ahead of the IRS in priority. This can make refinancing possible when it otherwise wouldn’t be. The IRS agrees to subordination when it believes doing so will ultimately help them collect, for example, if refinancing lowers your monthly payments and frees up cash for tax payments.

5. Offer in Compromise. If the IRS accepts your offer to settle the debt for less than the full amount owed, the lien is released once the offer terms are satisfied. Acceptance rates on Offers in Compromise have hovered around 30% to 40% in recent years, and the process typically takes 6 to 12 months. Our firm has written a detailed walkthrough of the Offer in Compromise process and what makes one successful.

The 10 Year Clock

A federal tax lien doesn’t last forever. The IRS has 10 years from the date of assessment to collect. This is called the Collection Statute Expiration Date (CSED). Once the CSED passes, the lien expires and the IRS must release it. However, certain actions can extend that clock: filing for bankruptcy, submitting an Offer in Compromise, requesting certain installment agreements, or living outside the country all pause or reset the timer.

Knowing your exact CSED for each tax year is critical to choosing the right resolution strategy. In some cases, a currently not collectible status makes more sense than an installment agreement specifically because it avoids extending the statute. This is the kind of analysis that requires someone who works with IRS collections regularly. If you have a revenue officer assigned to your case, the stakes are even higher, and you should consider professional representation before responding.

When to Act

The best time to deal with a lien is before one gets filed. If you’ve received a CP14 or any balance due notice from the IRS, you’re already in the escalation sequence. Setting up a compliant payment arrangement early, particularly a direct debit installment agreement for balances under $25,000, can prevent the IRS from filing the Notice of Federal Tax Lien in the first place.

If a lien has already been filed, the options above are real and available. But they require specific filings, documentation, and often negotiation with IRS collections. The difference between a lien that derails your finances for a decade and one that gets resolved in months usually comes down to how quickly you act and whether the approach matches your specific situation.

If you have a federal tax lien or owe back taxes you can’t pay, contact Austin & Larson Tax Resolution to discuss which resolution path fits your circumstances.

FAQs

How long does a federal tax lien stay on my record?

The IRS can enforce a federal tax lien for 10 years from the date your tax balance was assessed, which is known as the Collection Statute Expiration Date. Certain actions like filing bankruptcy or submitting an Offer in Compromise can pause or extend that 10 year window.

Will a tax lien show up on my credit report?

The three major credit bureaus stopped including tax liens on consumer credit reports in 2018, but the lien remains a public record accessible through county recorder searches and title checks. Lenders, landlords, and employers conducting background checks can still find it, and it will appear on business credit reports.

Can the IRS file a lien if I’m on a payment plan?

Yes, the IRS can file a Notice of Federal Tax Lien even if you have an active installment agreement in place. However, if you set up a direct debit installment agreement and owe $25,000 or less, you may qualify to have the lien withdrawn after making three consecutive on-time payments.

What is the difference between a lien release and a lien withdrawal?

A lien release means the IRS removes the lien because the tax debt has been fully paid or the collection statute has expired. A lien withdrawal removes the public Notice of Federal Tax Lien entirely, as if it was never filed, which is significantly better for your financial record.

Can I sell my house if the IRS has a lien on it?

You can sell your home, but the IRS lien must be addressed before or during the sale because the title company will not issue clear title with an active lien. The IRS may agree to discharge the lien from the property so the sale can proceed, with the tax debt paid from the closing proceeds.

Does the lien amount go down as I make payments?

No, the amount recorded on the Notice of Federal Tax Lien stays at the original balance from when it was filed regardless of how much you’ve paid since. The lien is not released until the full tax debt across all periods covered by that lien has been completely satisfied.

Recent Comments