In fiscal year 2024, one IRS program generated $7.7 billion in additional tax assessments. That program runs without a single human examiner touching it. The Automated Underreporter system flags mismatches between your return and third party data. Most taxpayers had no idea a problem existed until a notice arrived.

At Austin & Larson Tax Resolution, we represent clients through every type of IRS problem. We’ve handled forgotten 1099s that triggered CP2000 notices. We’ve resolved six years of unfiled returns with balances exceeding $180,000. The pattern repeats itself nearly every time. The problem started small, got ignored, and compounded fast.

This guide covers where IRS problems actually come from. You’ll learn which types escalate fastest. We break down the specific resolution paths available for each situation. That includes dollar thresholds, deadlines, and qualification criteria.

How the IRS Catches Problems Before You Know They Exist

The IRS doesn’t wait for you to make a mistake. Your financial data arrives at the IRS before your return does. Employers submit W-2s. Banks send 1099-INTs. Brokerage firms file 1099-Bs. Payment processors like PayPal and Venmo issue 1099-Ks. Cryptocurrency exchanges now report transactions on the new Form 1099-DA.

When you file, IRS computers check your return against every piece of third party data. If your reported income doesn’t match, the system flags the discrepancy automatically. Roughly 95% of income mismatches result in some adjustment to the return.

This automated matching is the single most common origin of IRS problems. Not fraud. Not aggressive deductions. Simple discrepancies between what you reported and what others reported.

The question isn’t whether the IRS will find the problem. The question is whether you’ll address it on your terms or theirs.

The Six Most Common IRS Problems

1. IRS Notices Requesting Additional Information

This is the mildest IRS problem and the one we see most often. The IRS sends a notice asking you to verify something on your return. They may need proof of a dependent, mortgage interest documentation, or business deduction support.

This is not an audit. It’s a clarification request. Responding with the right documentation within 30 days usually resolves it completely.

The problem starts when people don’t respond. The IRS then assumes the deduction was wrong. They adjust your return and send a bill for additional tax plus penalties.

What to do: Read the notice carefully. Each one has a specific notice number in the upper right corner. Gather the documents they request. Respond by the deadline printed on the notice. Keep a copy of everything you send. If you mail your response, use certified mail with a return receipt.

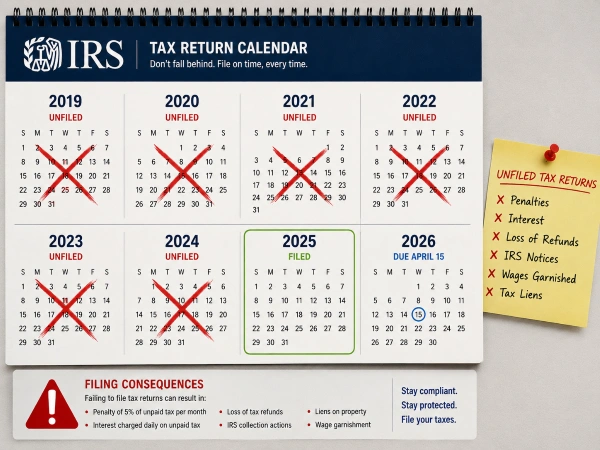

2. Unfiled Tax Returns

This is where the snowball effect hits hardest. A taxpayer owes more than expected one year. They can’t afford to pay, so they don’t file. The next year, the anxiety makes filing feel even harder. Fast forward five years and multiple unfiled returns create a massive balance.

The real danger comes from Substitute for Returns (SFRs). The IRS prepares these returns without your deductions, dependents, or credits. They use the least favorable filing status available. The resulting balance is almost always dramatically higher than your actual liability.

We’ve seen SFRs generate balances of $40,000 when the actual liability was under $8,000. That gap can destroy your financial stability.

What to do: File the returns even if you can’t pay. The failure to file penalty runs at 5% of unpaid tax per month, capped at 25%. The failure to pay penalty is only 0.5% per month. Filing your own return almost always produces a lower balance. You also cannot access any tax relief program until all required returns are filed.

3. Unpaid Tax Balances

Owing the IRS money you can’t pay immediately is stressful. However, this IRS problem actually has the most resolution options available. The IRS prefers collecting something over time rather than chasing silent taxpayers.

The failure to pay penalty runs at 0.5% of the unpaid balance per month. Interest accrues at approximately 8% annually in 2026. On a $20,000 balance, that means roughly $133 per month in interest alone.

Without action, the IRS follows a predictable escalation path. Notices come first. Then a notice of intent to levy arrives. Next comes a federal tax lien filing that damages your credit. Finally, wage garnishment or bank account levies begin.

What to do: Contact a tax professional before the IRS escalates to liens and levies. Resolution options improve significantly when you engage proactively.

4. IRS Audits

The word “audit” triggers more anxiety than almost any other tax term. Context matters though. The overall individual audit rate sits below 1% for most income levels. Three quarters of all audits are correspondence audits handled entirely by mail.

Certain profiles draw disproportionate attention from the IRS. Taxpayers earning over $500,000 face audit rates of 1% to 2%. Above $10 million, rates climb to roughly 8.5%. Self employed filers reporting Schedule C losses also face elevated scrutiny. The IRS uses its Discriminant Information Function (DIF) scoring system to flag these returns.

Other common triggers in 2026 include large charitable deductions relative to income. Home office deductions raise flags, especially for W-2 employees. Cash intensive businesses draw attention. Unreported cryptocurrency transactions trigger reviews now that exchanges issue Form 1099-DA.

What to do: Don’t panic, but don’t delay either. The IRS notice will specify what they want to examine. The response deadline is firm. Ignoring an audit means the auditor denies every unsubstantiated expense. They may also expand the audit scope to other years. For office or field audits, professional representation helps protect your interests.

5. IRS Penalties

The IRS assesses penalties for dozens of infractions. Three account for the vast majority of penalty revenue. The failure to file penalty charges 5% of unpaid tax per month, capped at 25%. The failure to pay penalty charges 0.5% per month, capped at 25%. The accuracy related penalty charges 20% of any underpayment from negligence.

Many taxpayers don’t realize that penalty relief exists. First Time Penalty Abatement (FTA) removes failure to file and failure to pay penalties. You qualify if you’ve filed on time, paid on time, and avoided penalties for three straight years. You can call the IRS directly and request it.

If you don’t qualify for FTA, you can request reasonable cause abatement. Valid reasons include serious illness, natural disaster, or death of an immediate family member. These requests require documentation and a written explanation.

What to do: Check FTA eligibility before paying any penalty assessment. If your three year compliance history is clean, call the IRS. For larger penalties, a tax professional can evaluate your reasonable cause arguments.

6. Identity Theft and Fraudulent Returns

This problem is less common but uniquely frustrating. Someone files a return using your Social Security number and claims a fraudulent refund. You discover the problem when your legitimate return gets rejected.

The IRS identity theft backlog remains a persistent issue. In 2025, hundreds of thousands of taxpayers waited over 21 months for the IRS to resolve their cases.

What to do: File Form 14039 (Identity Theft Affidavit) immediately. Request an Identity Protection PIN for all future returns. If the process stalls beyond 30 days, contact the Taxpayer Advocate Service.

How to Resolve IRS Tax Debt: Your Specific Options

Resolution starts with one non negotiable step. You must file all required tax returns first. Current year estimated payments must also be current. The IRS won’t approve any resolution program until you meet these conditions.

We see people make a costly mistake here constantly. They pour all available cash into the old balance. Meanwhile, they fall behind on current year taxes. This creates a brand new liability while trying to resolve the old one. Pay your current taxes first. Then address the back debt through one of these programs.

Installment Agreements (Payment Plans)

This is the most common resolution path. Approval rates exceed 90% for qualifying taxpayers. The IRS offers several tiers based on your balance.

- Guaranteed Installment Agreement: You owe $10,000 or less in combined tax, penalties, and interest. The IRS must grant this agreement. No financial disclosure is required. You agree to pay within three years.

- Streamlined Installment Agreement: Individual taxpayers who owe $50,000 or less qualify for this option. You can apply online through the IRS Online Payment Agreement tool. Approval is often immediate. Payments spread over up to 72 months.

- Non Streamlined Installment Agreement: Balances exceeding $50,000 require full financial disclosure. You’ll submit Form 433-A or 433-F. Setup takes longer, but the IRS still widely approves these agreements.

One important detail gets overlooked often. Entering an installment agreement reduces the failure to pay penalty rate. It drops from 0.5% per month to 0.25% per month automatically. Setup fees range from $22 for online direct debit agreements to $225 for phone or mail setup.

Offer in Compromise

An Offer in Compromise (OIC) lets you settle tax debt for less than you owe. The IRS acceptance rate hovers around 33% of processed applications. Knowing whether you’re a realistic candidate before applying saves time and money.

The IRS calculates your Reasonable Collection Potential (RCP). This factors in your monthly disposable income, asset equity, and time left on the collection statute. Your offer must meet or exceed the RCP to gain approval.

- Who this works for: Fixed income retirees, taxpayers with significant permanent income loss, and individuals with disabilities. People whose tax debt dramatically exceeds their earning potential also qualify. High income earners with substantial assets rarely qualify.

- The cost: A $205 application fee plus a nonrefundable initial payment accompanies Form 656. Lump sum offers require 20% upfront. Low income taxpayers can request a fee waiver.

- Our recommendation: Use the IRS Offer in Compromise Pre-Qualifier tool first. Then have an Enrolled Agent or CPA run the actual RCP calculation before filing. Learn more about whether an OIC is right for your situation.

Currently Not Collectible Status

If paying any amount would jeopardize basic living expenses, you may qualify for CNC status. The IRS pauses active collection but the debt remains. Interest and penalties continue to accrue.

CNC buys time. The IRS has a 10 year collection statute. If that statute expires while you’re in CNC status, the debt gets written off legally. The IRS will periodically review your finances. If your income improves substantially, they may resume collection.

Partial Payment Installment Agreement

This underused option works for taxpayers who can afford some monthly payment. However, they can’t pay the full balance before the collection statute expires. You make reduced monthly payments based on actual ability to pay. The remaining balance at statute expiration gets written off.

Resources When You Can’t Afford Professional Help

- Taxpayer Advocate Service (TAS): This independent IRS organization helps taxpayers facing financial hardship. Call 877-777-4778 or file Form 911 to request assistance.

- Low Income Taxpayer Clinics (LITCs): These clinics provide free or low cost IRS dispute representation. Find a clinic near you by calling 800-829-3676.

- IRS Online Account: You can view your balance, payment history, and transcripts at IRS.gov/account. You can also set up payment plans online without calling.

Take the First Step Before the IRS Takes the Next One

Every IRS problem has a resolution path. Installment agreements carry approval rates above 90%. First Time Penalty Abatement requires nothing more than a phone call for qualifying taxpayers. Even Offers in Compromise settle debts for pennies on the dollar when circumstances warrant it.

The variable that determines your outcome more than anything else is timing. Taxpayers who engage proactively land in a better position every time. Filing returns before the IRS sends notices makes a difference. Setting up payment plans before liens appear protects your credit. Responding to audit letters before deadlines pass preserves your rights.

If you’re dealing with an IRS problem right now, contact our office for a free consultation. We’ll evaluate your situation, walk you through your options, and take action before deadlines expire. You can also learn more about how the tax relief process works before your first call.

FAQs

What should I do first when I receive an IRS notice?

Read the notice immediately and check the notice number in the upper right corner. Respond by the printed deadline with the specific documents the IRS requests.

Can the IRS file a tax return on my behalf?

Yes, the IRS can file a Substitute for Return (SFR) that excludes your deductions, credits, and dependents. This almost always creates a much higher tax balance than filing your own return would produce.

What is the difference between a tax lien and a tax levy?

A tax lien is a legal claim the IRS places on your property as security for unpaid tax debt. A tax levy is the actual seizure of your wages, bank accounts, or other assets to satisfy that debt.

How long does the IRS have to collect tax debt?

The IRS has 10 years from the assessment date to collect. After this Collection Statute Expiration Date passes, the IRS cannot legally pursue the remaining balance.

Will the IRS accept monthly payments if I can’t pay my full tax bill?

The IRS offers several installment agreement options for taxpayers who can’t pay in full. Taxpayers owing $50,000 or less can often set up a plan online in minutes.

What is an Offer in Compromise and who qualifies?

An Offer in Compromise lets you settle IRS tax debt for less than you owe. You typically qualify if your finances show you genuinely cannot pay the full balance.

Can I lose my home or car if I owe the IRS?

The IRS can seize property, but this is relatively uncommon for most taxpayers. Engaging proactively through a payment plan or resolution program almost always prevents asset seizure.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments