Written By: Michael Vale

Reviewed By: Bridgette Austin, Esq., EA, Co-Founder and Tax Attorney

Last Reviewed: May 20, 2026

IRS Currently Not Collectible status is a temporary designation that stops the IRS from collecting your tax debt when you prove you can’t afford to pay, not even in monthly installments. It doesn’t erase what you owe. It pauses enforcement actions like wage garnishments and bank levies while interest and penalties keep growing.

About 84.9% of taxpayers pay by the deadline. The rest face a system that most people don’t understand until they’re already in trouble. And the biggest mistake I see isn’t owing money. It’s doing nothing about it.

IRS Currently Not Collectible (CNC) status is one of several options for people who genuinely can’t pay. But it’s not the right move for everyone. If you have any disposable income after the IRS runs its calculations, you won’t qualify. And if you do qualify, you’re trading short-term relief for long-term cost.

This article covers exactly how CNC works, who actually qualifies, and whether it’s the smartest move for your situation in 2026.

What Is IRS Currently Not Collectible Status?

CNC is an IRS designation that tells the collection division to stop pursuing you temporarily. You still owe the debt. Interest still accrues. Penalties still stack. But the IRS won’t garnish your wages, levy your bank accounts, or seize property while the designation is active.

The IRS has a formal process for temporarily delaying collection that covers CNC. When you’re approved, your account gets coded with a specific transaction code (TC 53), and active collection stops.

One thing most people get wrong: CNC doesn’t stop the 10-year collection statute of limitations from running. That clock keeps ticking. If the IRS doesn’t collect within 10 years of assessing your debt, the balance expires. But the IRS reviews your finances regularly (usually annually), and they can pull you back into active collection any time your income improves.

Who Qualifies for CNC Status?

The IRS doesn’t publish a specific income threshold for CNC. Instead, they run your numbers through their Collection Financial Standards, which set allowable amounts for housing, food, transportation, and healthcare based on your county. If your income minus those allowable expenses equals zero (or less), you qualify.

That’s a higher bar than most people expect. The IRS doesn’t care about your Netflix subscription. They care about rent, basic utilities, food within their published limits, and minimum payments on secured debts. Everything else is disposable income.

You might qualify if you’re:

- Self-employed with irregular income that doesn’t cover basic living costs

- On Social Security with a small side income that creates a tax liability

- Collecting unemployment while carrying expenses the IRS considers necessary

- Dealing with a medical situation that has drained your savings

Here’s something people rarely mention. The IRS updated its Collection Financial Standards in 2025 with roughly 5% increases across most regions due to inflation. If you were denied CNC in 2023 or 2024, the math may work differently now. A taxpayer in a high-cost county near San Francisco will qualify at income levels that would disqualify someone in rural Oklahoma. The NATP published a useful guide on how to document a taxpayer’s financial hardship for CNC specifically. That regional gap in hardship standards is one of the most underreported parts of the process.

How Do You Apply for CNC Status?

You have to contact the IRS directly. There’s no online form you can submit.

If you’ve received a notice, call the number printed on it. If you don’t have a notice, call 800-829-1040 for individual taxpayers (TTY/TDD 800-829-4059) or 800-829-4933 for businesses.

The IRS may require you to:

- File all past-due tax returns before they’ll consider your request

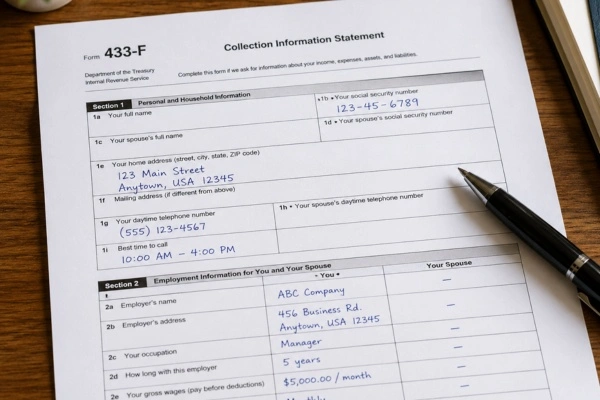

- Complete Form 433-F (Collection Information Statement) or Form 433-A if you’re self-employed

- Provide backup documentation for every line item on that form

One significant change in 2025: the IRS launched its Digital Correspondence Initiative, letting you upload Form 433-F through a secure online portal instead of mailing everything. This cut average CNC review time from about 8 weeks to roughly 5 weeks.

During the review, the IRS agent might suggest alternatives. An installment agreement works if you can afford monthly payments and owe less than $50,000. A short-term plan (up to 180 days, no setup fee) works if you just need a few months. And if your situation is permanently bad, an Offer in Compromise might settle your debt for less than you owe.

What Documents Does the IRS Need for a CNC Application?

Incomplete documentation is the number one reason CNC requests get denied. The IRS wants proof, not estimates.

Expect to gather:

- Recent pay stubs or profit-and-loss statements for self-employment income

- Your most recent property tax bill or lease/rent payment record

- Utility bills and insurance statements

- Auto loan, credit card, and other debt statements

- Bank statements showing account balances

- Proof of monthly expenses for food, transportation, childcare, medical costs, and court-ordered payments

The IRS also caps certain expenses. They limit how much you can claim for a monthly car payment based on local standards. If you’re paying $800/month on a car when the IRS allows less for your area, they’ll use their number. These standards are published on IRS.gov and vary by county.

I always tell clients to keep organized records year-round, not just when the IRS comes calling. Scrambling to reconstruct six months of expenses from memory means leaving money on the table.

Benefits of Currently Not Collectible Status

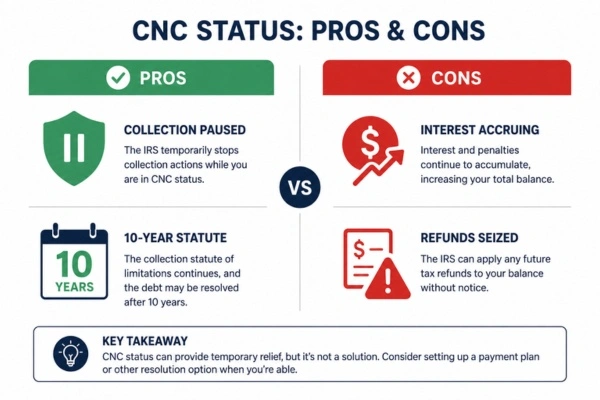

CNC gives you breathing room when nothing else works. The IRS stops collection activity, which means no levies, no garnishments, and no threatening letters while the designation holds.

The biggest upside is the statute of limitations. The IRS has 10 years from the date of assessment to collect. CNC doesn’t pause that clock. If your finances never recover and you ride out the full 10 years, the IRS writes off the remaining balance, including penalties and interest. That’s a real outcome for people with permanent disabilities, chronic illness, or fixed retirement income.

For someone who owes $25,000 with only 4 years left on the statute, CNC can be the most strategic option available. For someone with 9 years left on a $40,000 balance, the math gets ugly once you factor in accruing penalties.

What Are the Real Downsides of CNC?

CNC is a pause, not a solution. And the costs of pausing add up.

Interest and the failure-to-pay penalty (0.5% per month, up to 25% of the balance) keep running the entire time. On a $20,000 balance, those charges alone can add thousands over a few years.

The IRS will also offset your refunds. Any future tax refund gets applied to your balance automatically while you’re in CNC.

Your status isn’t permanent. The IRS reviews your finances periodically. A raise, an inheritance, or a new job that pushes your income above the threshold means they’ll pull you out of CNC and resume collection.

And if you owe more than $10,000, the IRS can still file a Notice of Federal Tax Lien against your property. That lien makes it harder to sell a home, refinance, or get approved for new credit.

Which IRS Relief Option Is Right for You?

Most people who call about CNC are better served by one of the other two options:

CNC is the right call when you truly have nothing left after basic expenses. If you have even $100/month in disposable income, the IRS will push you toward an installment agreement. If your financial situation is permanently bad, an Offer in Compromise may actually reduce what you owe.

The Taxpayer Advocate Service published an April 2026 guide covering payment options when you can’t pay federal taxes in full. Worth reading before you decide.

One contrarian take: I think CNC is overused by national tax relief companies because it’s the easiest case to close. Getting someone an Offer in Compromise takes months and requires real work. If a firm is pushing CNC without even running your OIC numbers, that should raise a red flag. Working with experienced tax resolution attorneys in Michigan means all three options get evaluated before anyone recommends one.

Talk to a professional who can help you resolve your IRS tax debt before applying for anything.

FAQs

Does IRS Currently Not Collectible status forgive your tax debt?

No. CNC only pauses active IRS collection. You still owe the full balance, and interest plus penalties keep accruing the entire time. The failure-to-pay penalty alone adds 0.5% per month, up to 25% of your total balance. The only way CNC leads to debt elimination is if the 10-year collection statute of limitations expires before the IRS resumes collection.

How long does CNC status last?

There’s no fixed timeframe. CNC lasts until the IRS decides you can pay or until the 10-year statute runs out. The IRS reviews your financial situation periodically (usually once a year) and can revoke your CNC designation at any time if your income increases.

Can I apply for Currently Not Collectible status without hiring a tax professional?

Yes. You can call the IRS directly and submit Form 433-F yourself at no cost. Many taxpayers handle this successfully on their own. That said, professional help improves documentation quality. Practitioners report roughly 80% CNC approval rates when submissions include complete financial records, compared to significantly lower rates for incomplete DIY filings.

Will the IRS still take my tax refunds while I’m in CNC?

Yes. The IRS typically offsets any future refunds against your outstanding balance, even with CNC status active. If you normally receive a $2,000-$3,000 refund each year, plan on that money going to your tax debt until the balance is paid or the statute expires.

What triggers the IRS to remove CNC status?

The IRS can pull you out of CNC if your income rises, you file a return showing higher earnings, you inherit assets, or a periodic review shows you now have disposable income above their allowable expense thresholds. A new job, a raise, or even a spouse’s income change can trigger it.

Is CNC better than an Offer in Compromise?

It depends on whether your hardship is temporary or permanent. CNC works best for temporary situations where you have zero disposable income right now but may recover later. An Offer in Compromise works better when your financial situation is unlikely to improve, because it actually settles the debt for less. The National Association of Tax Professionals recommends using Form 433 analysis to determine which path fits.

Can I stay in CNC until the 10-year collection statute expires?

It’s possible, but not guaranteed. The IRS has 10 years from the date of assessment to collect, and that clock keeps running during CNC. If your financial situation never improves, the balance (including accrued penalties and interest) expires when the statute runs out. The IRS reviews your finances periodically, though, and can pull you back into active collection at any point. For someone with only 3-4 years left on the statute, this is a realistic path. For someone with 8-9 years remaining, the odds of riding it out without an income change are much lower.

Bridgette Austin, Esq., EA, spent three years at Michigan State University’s Tax Clinic representing low-income taxpayers before the IRS – two as a student clinician, one as a post-graduate fellow. That work shaped her practice. A Bellaire, Michigan native with a Northern Michigan University bachelor’s and an MSU law degree, she now resolves IRS and State of Michigan tax debt cases at Austin & Larson.

Recent Comments